Continued double-digit growth in rail freight between Asia and Europe is prompting Europe to invest in infrastructure. This article reviews the main emerging projects and their potential.

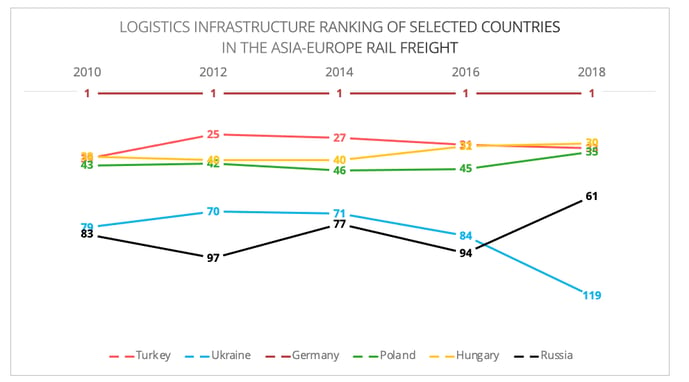

By crossing the threshold of 50,000 train trips made since the launch of the services in 2011, rail freight between China and Europe reached a new milestone in January 2022. However, the discrepancy between the exponential growth and an infrastructure development that is lagging and asymmetrical is hindering the long-term growth (Figure 1). Congestion at the Polish hub of Małaszewicze, aggravated by the current supply chain disruptions, has generated growing demands for alternative options, an opportunity that European countries are now trying to seize.

Figure 1- Data Source: World Bank Logistics Performance Index

Overview of the Investment in Infrastructure

Overall, investments in rail freight infrastructures can be divided into two categories: those that will finance alternative routes and those that will increase capacity at the current main border crossing points (Table 1).

Table: Selected Infrastructure Investment Projects. Information generated based on various media sources.

New Routes

New routes via Ukraine and Turkey have gained significant interest from European and Asian investors. The Austrian railway operator ÖBB is actively engaging in both options.

- Ukraine: Alternative Border Crossings

Ukraine’s geographic location incites its EU neighbours to invest in infrastructure aimed at attracting Asian flows to enter the EU via the border crossings with Ukraine.The conflict with Russia, however, is likely to affect the many promising projects for a long time to come.

The agreement between China and Ukraine signed in July 2021 to upgrade the transportation infrastructure when coupled with the new rail freight route between Xi’an and Kyiv may have further boosted the market interest to develop the Asia-Europe route via Ukraine.

The Záhony region on the Hungary/Ukraine border is at the centre of Hungary’s ambition to become the main transport hub connecting Asia and Europe. 2021 saw a growth of flow via this region. Last year, around 100 rail freight trains from China entered the EU via Záhony, whereas in 2020 the number was only 34. Specifically, Hungary is keen to develop the multimodal connections between China and Southern Europe and the Balkans via Russia and Hungary through the recent joint venture between Russian Railways Holding, CER Cargo Holding (Hungary), and Rail Cargo Group (Austria).

One critical infrastructure project in this region is the East-West Gate Terminal (EWG) in Fényeslitke, which is likely to open in the second quarter of 2022. The EWG, with a capacity of 1 million TEUs per year, will be the largest intermodal terminal with 5G facilities in Europe.

Investors are also eying the Poland and Ukraine border crossing. The Polish railway company PKP plans to expand its terminals in Medyka to make this region the second Małaszewicze. On the other side of Medyka is the Mostyska terminal in Ukraine, which is scheduled to open in April 2022. By offering both broad and standard gauges, the Mostyska Terminal could attract rail freight between Asia and Europe. But of course, with the conflict that broke out on 24 February, there is now total uncertainty about this project, as with all rail freight projects involving Ukrainian territory.

- Turkey: Hub of the Middle Corridor

Turkey maintains its vision as a logistics hub connecting Asia and Europe. Specifically, Turkey aims to capture 30% of the flows that today pass through the North corridor via Russia thus switching them to the Europe-Caucasus-Asia Corridor (Middle Corridor). This route has attracted both European and Asian investors. For instance, in June 2021, ÖBB paired with Eurasia Pacific to offer a multimodal solution via the Middle Corridor where Köseköy links Asia and Europe.

An integral part of the Middle Corridor, the € 300 million Ispartakule-Cerkezkoy railway project, was approved in September 2021. Jointly financed by the Asian Infrastructure Investment Bank and the European Bank for Reconstruction and Development, this rail freight link will connect the Turkish rail network to the trans-European transport network via Bulgaria, making it more attractive to Asian flows.

Besides International investment, the Turkish Ministry of Transportation and Infrastructure also plans to increase the share of rail in its investments to 60%. Turkey hopes, through intensive investment, to operate 1,500 block trains per year from the Middle Corridor and Baku-Tbilisi-Kars route and thus shorten the shipping time from China to Turkey from the current 12 days to 10 days.

Infrastructure Upgrading on Main Routes

Alongside the development of alternative routes is the effort to upgrade main border crossings to maintain competitiveness.

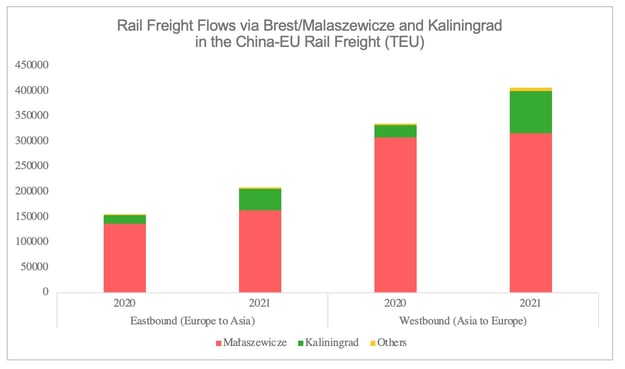

In 2021, Małaszewicze suffered a significant market loss (Figure 2). Its share in China-Europe rail freight has dwindled from 90% in 2020 to 77% in 2021[1]. Capacity expansion, therefore, becomes essential to maintain its status as the primary border crossing. A flagship project is the logistics park undertaken by Cargotor, the subsidiary of PKP. The planned logistics park will cover 30 square kilometres. The feasibility study also foresees an improvement of local roads including crossings over the railway tracks in Kobylany and Zaborze. However, this project is not expected to be completed before 2027/2028.

Figure 2 - Data Source: ERAI 1520 Statistics[2]

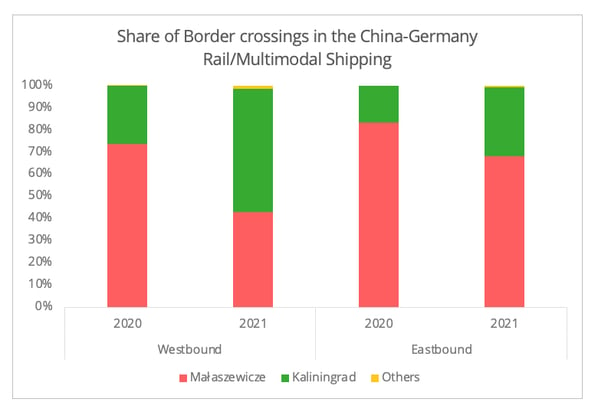

Małaszewicze's loss of market share in 2021 was to the benefit of Kaliningrad, especially for shipments between China and Germany. Last year, 58% of westbound China-Germany rail freight passed through Kaliningrad, which thus became the main border crossing point for these flows by overtaking Małaszewicze (Figure 3). However, the sharp increase in shipments also caused delays on this route. To expand the capacity, a new logistics centre, "East-West," was opened in October 2021, aiming to increase the capacity of the Chernyakhovsk station in Kaliningrad to 450,000 TEUs per year.

Figure 3 – Data Source: ERAI 1520 Statistics

The Birth of another Kaliningrad?

Undoubtedly, these projects will provide multiple options for the China-Europe rail freight and for the multimodal connection between Southeast Asia and Europe via China. But let us take our analysis a step further. Is the success of Kaliningrad replicable? Surely, all these infrastructures are targeting Asian, and more specifically Chinese flows. But are they attractive enough for the China-Europe trade? The answer is… yes and no.

Currently, flow through Germany and Poland make up around 85-90% of all China-Europe rail freight. While tight capacity at main border crossings can divert shipping demand to other routes, long-term prospects for these projects will be dependent on whether the rail freight sector can cultivate new markets. This will be conditioned by two factors: the trade demand and the modal shift demand to divert to rail freight.

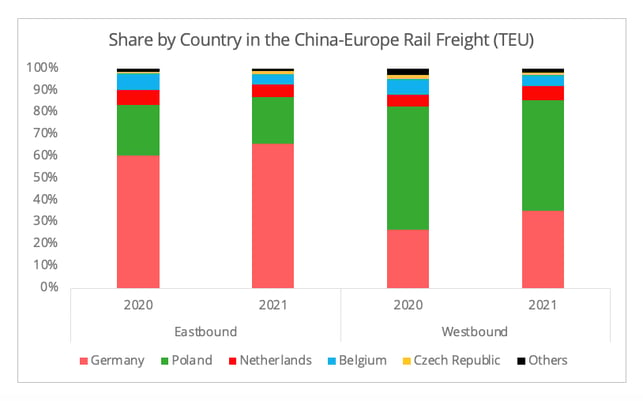

The success of Kaliningrad fits both conditions. Firstly, it emerged at an ideal moment: in the middle of logistics disruption when well-equipped alternative options were scarce. Therefore, there was an urgent need for modal switch. Secondly, the site itself is an optimized option for the China-Germany trade, which accounted for 45% of rail freight between China and Europe in 2021 (Figure 4), indicating dynamic trade activity.

Figure 4 - Data Source: ERAI 1520

Can these conditions be met in these new projects? Perhaps one positive note regarding demand for modal shift is the target set by the EU to double rail freight traffic by 2050 under the current Sustainable and Smart Mobility Strategy. Let us briefly analyse the cases of Hungary and Turkey on the basis of this framework.

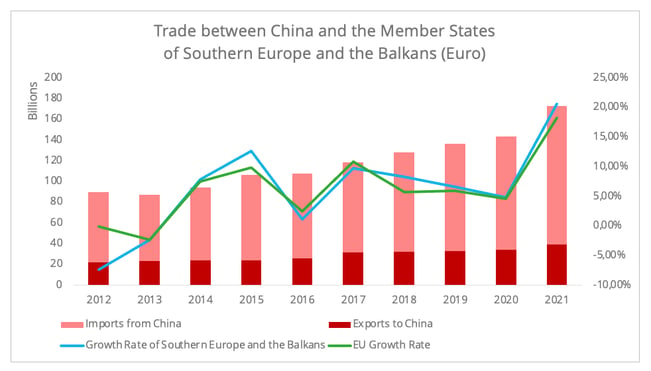

In the Hungarian case, the newly formed joint venture between Hungarian, Austrian, and Russian rail sectors showed a clear interest in developing the rail freight connections of Southern Europe and the Balkans with China. Currently, the share of this region in China-Europe rail freight remains marginal. However, the slightly higher growth rate of the trade between China and this region against that between China and the EU since 2018 indicates the potential for this demand.

One factor in particular is likely to generate growing rail freight demand: Eastern Europe and Spain are at the heart of China's cross-border e-commerce development strategy in Europe. This sector is increasingly seeking to integrate with rail freight.

However, the route linking Asia to Southern Europe and the Balkans may need to compete with another China-initiate multimodal shipping project, the China-Europe Land-Sea Express (Ocean freight to Greece and then rail freight to Europe) operated by COSCO. This route in 2021 operated 153,000 TEUs, showing a 25.2% annual growth.

Figure 5 - Data Source: Eurostat

- Turkey and the Middle Corridor

Turkey's attractiveness as a nearshoring option for the European market could generate increasing demand from both Europe and Asia. In particular, Turkey as a popular destination for textile nearshoring could also attract Chinese flow since China remains the world's largest supplier of intermediate textile goods. By 2020, China accounted for around 18% of Turkey’s total imports of intermediate textile goods[3]. Furthermore, the recent flood in Chinese investment from the mobile telephone sector in Turkey may also generate new logistics demand for intermediate machinery goods between China and Turkey.

However, Turkey’s potential as a logistics hub for the Asia-Europe rail freight is also influenced by China’s transport policy. China-Europe rail freight, since day one, is a largely policy-driven project. For Chinese local authorities, the policy instructions of the central government predominately shape their decision-making in the development of new routes. Indeed, the China-Central Asia-Western Asia route was listed among other flagship projects in the Chinese National Comprehensive Transport Network issued in 2021. However, it may denote a stronger Chinese interest in using Turkey to connect with the broader Western Asian region rather than just as a connecting point to reach Europe.

At the same time, two factors will shape the long-term potential of these options.

- Long-term Interest and Short-term Disruption

Clearly, efficient infrastructure is crucial in securing long-term growth. However, short-term disruptions due to construction sometimes alter the services and therefore long-term benefits. Congestion at border crossings caused by expansion projects have been reported from time to time.

Apart from border crossings, the asymmetrical development of infrastructure across the countries on the route is another salient issue. Taking Ukraine as an example, its infrastructure is significantly lagging behind that of its neighbours (Figure 1). The Ukrainian Ministry of Infrastructure estimated that 97% of the rolling stock requires modernization or replacement. Although both European countries and China are investing in the domestic rail freight infrastructure in Ukraine, major upgrading cannot be done overnight.

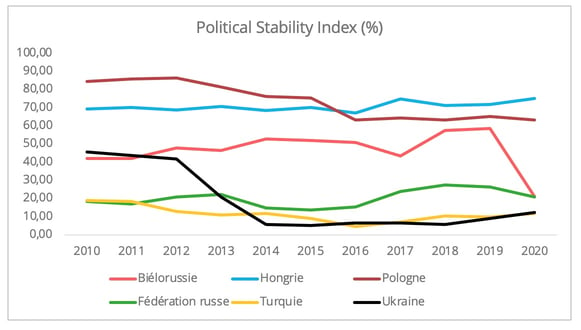

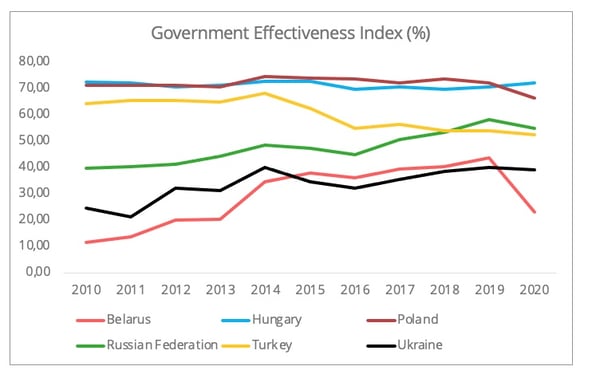

One cannot not neglect the political factors deeply embedded in the areas where the above mentioned infrastructure projects are taking place. This region suffers from political instability and low effectiveness of governance (Figure 6 & 7). The red tape cost due to the less effective governance will hamper operations on these routes.

Figure 6- Data Source: The Worldwide Governance Indicators, World Bank[4] [5]

Figure 7- Data Source: The Worldwide Governance Indicators, World Bank[6]

More critically, the complex political scenario lowers the predictability of the utilization of these routes. Rail freight operation, therefore, can be sacrificed or become an instrument in political disputes. For instance, the shutting down of the Małaszewicze terminal was on the table amid the border crisis between Poland and Belarus in November 2021. Furthermore, the three-month shipping ban (11/2021 02/2022) from the Ukrainian side of trains to and from Poland transiting through its borders inexorably makes people question the border crossing liability via Ukraine.

Finally, the alternative option of a border crossing via Ukraine is largely overshadowed by the current crisis between Ukraine and Russia. Escalating tensions have led some operators to temporarily divert shipments or suspend China-Europe rail freight operations via Ukraine. Such political strategic concerns may also curtail China’s interests in developing routes via Ukraine, at least for now.

[1] If not specified, all the shipping volume data in the paper refer to TEUs and is based on the ERAI 1520 Statistics.

[2] The Freight volume of Brest includes Brest-center and Brest-Severny, and the freight volume of Kaliningrad includes Kaliningrad-Sortirovochniy, Mamonovo, and Baltiysk from the database.

[3] This is calculated based on the End-Use Database from OECD.

[4] Both rankings are percentile ranks among all countries (ranges from 0 (lowest) to 100 (highest) rank).

[5] This index measures perceptions of the likelihood of political instability and/or politically-motivated violence, including terrorism.

[6] The Government Effectiveness Index reflects perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government's commitment to such policies.