The China-Europe rail freight market is undergoing a major transformation, with the notable emergence of the Middle Corridor, despite significant operating constraints.

In 2023, in light of geopolitical uncertainties and a gloomy global economy, freight volumes on the new Silk Road Corridor via Russia (“Northern Corridor”) keep falling. At the same time, shipments via the Trans-Caspian trade corridor (“Middle Corridor”)- bypassing Russia– started to burgeon.

The Bleak Northern Corridor

In contrast to the fluctuations recorded in 2022, rail freight volumes remained relatively stable in 2023. By the 3rd quarter of 2023, volumes were 44% below the 2022 level in the eastbound direction (to China), and down 51% in the opposite direction (Figure 1). Besides the geopolitical uncertainties and collapse in ocean freight rates, the global slump in consumer electronic goods in particular, also took a toll on the westbound demand (to Europe). Electronic goods have long been the largest commodity in the westbound shipping.

Figure 1 - Data Source: ERAI

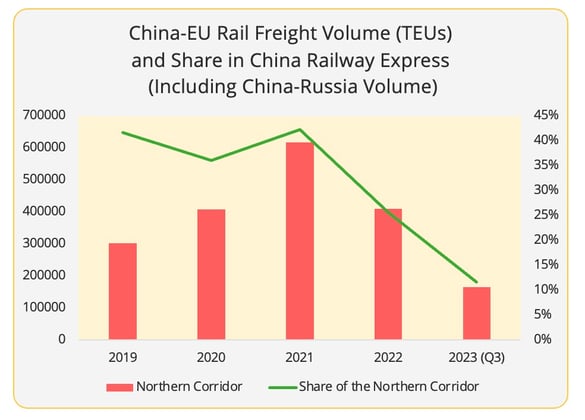

In the meantime, the exponential development of the China-Russia trade has led to a boom in shipments on this route. On the Northern Corridor, China-Russia trade has now overtaken China-EU trade as the dominant source of volumes for the China Railway Express (Figure 2).

Figure 2 - Data Source: ERAI and China Railway[1]

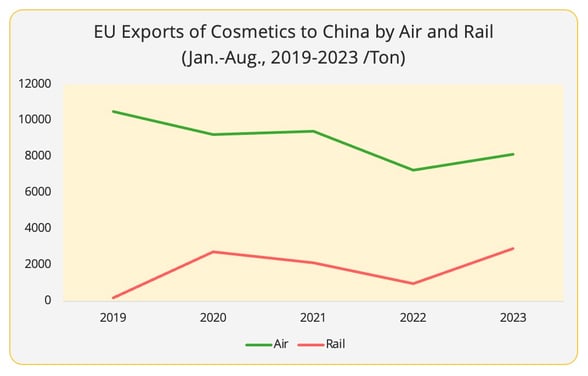

Amid the downturn of the rail freight market between China and the EU, the non-electronic consumer products have appeared to be more resilient. This is particularly true of products that can be linked to the post-pandemic resumption of social activities, such as the cosmetics and fashion industry, like textile and leather products.

Cosmetic products are the most significant example Eastbound with 1.7-fold growth in volumes (TEUs). The revival in social gatherings in post-pandemic China has contributed to the demand for make-up and skin care products. For example, L’Oréal has reported 7.7% growth in its sales in the Chinese market in the first three quarters of 2023. Apart from the recovery of market demand, the rise in rail freight volumes of cosmetics can also be partly attributed to the diversion from air freight (Figure 3). This sector, which is the other main shipping mode for cosmetics after sea freight, nevertheless remains above its pre-pandemic level.

Figure 3 - Data Source: Eurostat

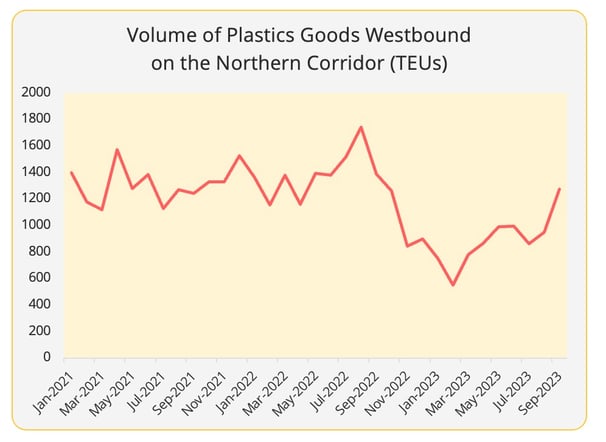

Similarly, among the top commodities Westbound, plastics goods appeared more resilient and showed better signs of recovery. For example, plastic goods in September 2023 had already reached the pre-Russia-Ukraine war level (2021), though less than 2022's volume (Figure 4).

Figure 4 - Data Source: ERAI

This also corresponds to the overall EU demand pattern for consumer products from China. After relentless efforts to reduce their excessive inventory, shippers are taking baby steps when restocking for the new holiday season (Figure 5).

Figure 5 - Data Source: European Central Bank

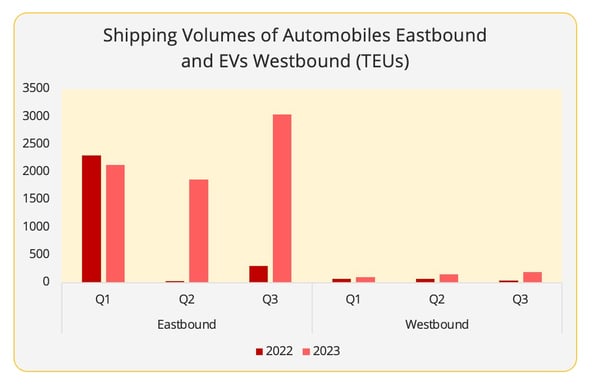

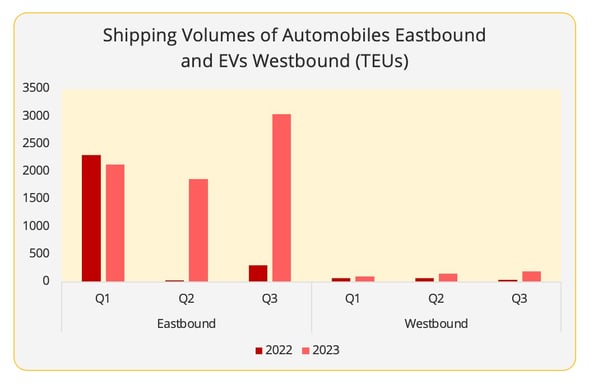

Passenger vehicles are another consumer product that saw positive growth in 2023. Particularly as rail transport to China of vehicles manufactured in Europe (mainly in Germany) has resumed, after having ceased completely in 2022 (Figure 6). Efforts have been made to restore shippers' confidence. However, volumes recovered remain below pre-war levels. The evolution of demand Westbound can be closely linked to the economic policies favoured by governments. Despite China's policy of supporting electric vehicle (EV) exports to Europe, rail volumes remain marginal compared with China's exponential exports of electric vehicles to the European market.

Figure 6 - Data Source: ERAI

The Development of the Middle Corridor

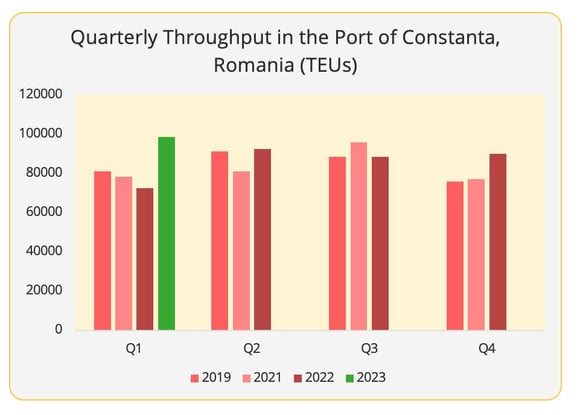

In contrast to the Northern Corridor, the Middle Corridor recorded favourable results this year. In the first half of 2023, it reported a 77% increase in tonnage, reaching 1.3 million tons. This dynamism can be observed in the surging throughput in the Port of Constanta in Romania since the fourth quarter of 2022, this port being the main entry point to the EU for the current Middle Corridor – from Poti in Georgia (Figure 7). Meanwhile, volumes on the Northern Corridor in tonnage have dropped by 56%. As a result, the gap between the two routes is narrowing. In the first half of 2023, volumes on the Middle Corridor represented around 18% of those on the Northern Corridor (tonnage[2]) compared with just 6% in 2022.

However, the future of the Middle Corridor still faces several challenges: long lead times (50-60 days), higher costs due to the multimodal nature of the route which induces load breaks, and additional administrative costs due to the greater number of countries crossed compared to the Main Route. As an outcome, despite bypassing Russia being an attractive option, this rail corridor does not offer significant advantages when competing with sea transport between Asia and Europe, given current operating conditions.

Figure 7 - Data Source: Eurostat

Outlook for the future

Looking forward, there is no doubt that geopolitical considerations will continue to create uncertainty in this market. For example, the new EU sanction package aimed at cracking down on the shipping of dual-use products via Russia has added additional compliance costs. At the same time, the rail freight between China and the EU is adapting to the collapse in ocean freight rates and the long-drawn-out war in Ukraine. Finally, the prospects for the rail freight market between China and the EU also reflect the state of the bilateral trade relations, the organization of supply chains, and economic strategies.

- The Future of the Northern Corridor

The positive demand on the Northern Corridor is likely to continue to be generated by the service consumption driven economy in both China and the EU. However, there are also some noticeable challenges ahead. Here, we will take the case of cosmetics as an illustration of this point.

The rising volume of trade in cosmetic products this year bears similarities to the increase in European milk powder volumes Eastbound in 2022. Both are consumer products with a strong Chinese demand for external supply and diverted volumes from air freight to rail freight due to the difference in their rates. These similarities may suggest that, under the current circumstances, goods are more likely to switch to rail when they meet the following three conditions: relatively high value added, strong Chinese demand from external suppliers, potential to capture air freight flows (competitiveness).

However, due to improved ocean shipping reliability and pessimistic consumer confidence forecasts, retailers are gradually shifting back to the “just-in-time” from the “just-in-case” inventory strategy. Under these conditions, the demand to rebuild the inventory will be conservative for both East and Westbound trade.

For example, the oversupply of the diary market in China and the record low number of newborns in China could explain the lack of milk powder demand via rail freight in 2023. As a matter of fact, the total Chinese demand for European milk powder has plunged.

Undoubtedly, the cosmetics market is more stable than milk powder. However, the rise of Chinese domestic cosmetics brands is challenging the long-term market prospects of imported skincare and make-up products. The challenge is similar for the imported vehicles Eastbound. Domestic brands have taken half of the Chinese vehicle market in 2022, squeezing the market share of foreign cars.

- The Future of the Middle Corridor

As for the development of the Middle Corridor, the interest shown by both the Chinese and European governments could drive the infrastructure improvement and shipping facilitation. In China's Belt and Road Initiative Summit in October, the Chinese government, for the first time, formally announced the development of the Middle Corridor. Since the outbreak of war, China and the EU have not shown the same degree of interest in developing the Middle Corridor. Europe is obviously more eager to tap into the Middle Corridor, which bypasses Russia. We can therefore expect to see the emergence of two types of market development models for the Middle Corridor.

The first type would be that EU-China shipment is primarily driven by public policy initiated by Chinese local governments implementing central government policy. This strategy has already been observed in the birth of the China-Europe rail freight market, particularly in the westbound direction, to serve the development of the Belt and Road Initiative.

The second type is more market-based, in line with the development of China's and the EU's trade with Central Asia. The current geopolitical tension has gravitated China and Central Asia closer. The latest Belt and Road Initiative Summit has sent a clear signal of China's market expansion in the Global South, which includes Central Asia. In the first three quarters of 2023, China's trade with Central Asia grew by 25%, mainly thanks to Chinese exports to this region. This trend can also be seen as part of China's diversification towards other export markets, at a time when the West is itself looking for alternative suppliers.

Likewise, in the recent Germany-Central Asia Summit, the German government expressed interest in jointly developing the Middle Corridor under the EU Global Gateway. Over the past four years, the EU-Central Asian trade has grown by 75% (in value), according to the Eurostat. The war in Ukraine has made securing alternative critical natural resources suppliers imperative, and the Middle Corridor has become an essential infrastructure project to underpin the EU’s economic diversification strategy.

[1] China Railway Express includes China-Central Asia, China-Russia, China-Belarus, China and the EU and other destinations on the Eurasian continent.

[2] Here we use tonnage due to the latest volume data of Middle Corridor in TEU is not available.