The global economy has entered a state of slowdown that particularly affected the Eurozone in 2023. In addition, supply-chain management must also integrate increasing geopolitical uncertainties.

The global economy experienced a further slowdown in 2023, confirming the trend seen since the second half of 2022, after a phase of strong recovery post-Covid that had started in the spring of 2021. On the one hand, inflation has started to decrease, which is good news for businesses’ production costs and for household purchasing power, but the process is slow and fragile. On the other hand, this is done at the price of an increase in credit costs that penalises investments.

In this context, the demand for goods has decreased, which has reduced the demand for transport and led to a decline in freight rates. The supply chain congestion phenomena observed in 2022 has largely been resolved, as have the episodes of component shortages.

The year 2023, on the other hand, confirmed the emergence of new patterns of globalisation, influenced by the multiplication of geopolitical crises.

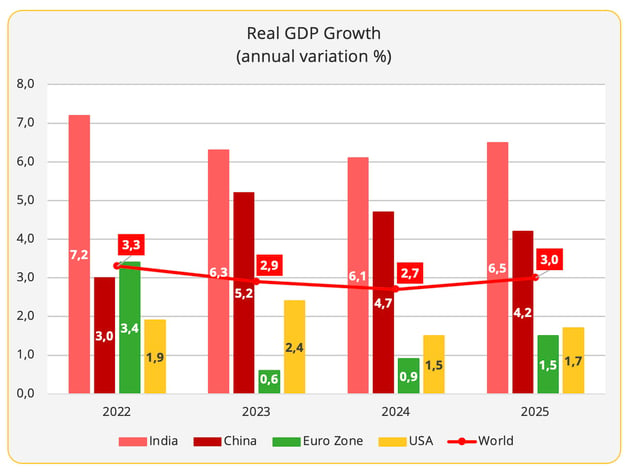

1/ Slow growth

Data source: OECD - © Upply

According to the OECD’s Interim Economic Forecast published in November 2023, world gross domestic product is expected to grow by 2.9% for the whole of 2023. This figure reflects a slowdown compared to 2022, and erosion is expected to continue in 2024, with growth falling to +2.7%.

In 2023, the economy turned out to be rather stronger than expected at the beginning of the year, thanks to lower energy prices and the reopening of China which ended its Zero-Covid policy. However, in the second part of the year, activity was penalised by the tightening of monetary policy aimed at fighting against inflation, as this policy weighed on the purchasing power of households and on the investment capacity of businesses.

The detail of GDP growth figures by major countries or major economic areas, however, shows significant disparities. India is experiencing a slowdown but is still leading in terms of growth rate. It is ahead of China, which has, for its part, experienced a clear rebound compared to 2022, but had, however, shown worrying signs in the second half of the year, particularly due to the serious real estate crisis affecting the country. The United States is also doing better than forecast, with GDP growth expected to be 2.2%, up from the 1.6% forecast in June. On the other hand, European performance was disappointing, with growth of 0.6% in 2023. The Eurozone is being hampered by the difficulties of its main economic powerhouse, Germany, which is expected to end the year with a GDP down 0.2%. The satisfactory results of France (+1%) and even more so Spain (+2.3%) mitigate the weakening, but this is not enough to breathe new life into the European economy, which is very dependent on Germany's health. “A growing divergence across economies is expected to persist in the near term, with growth in the emerging-market economies generally holding up better than in the advanced economies, and growth in Europe being relatively subdued compared to that in North America and the major Asian economies.” In 2024, the Eurozone is expected to record growth in GDP (+0.9%).

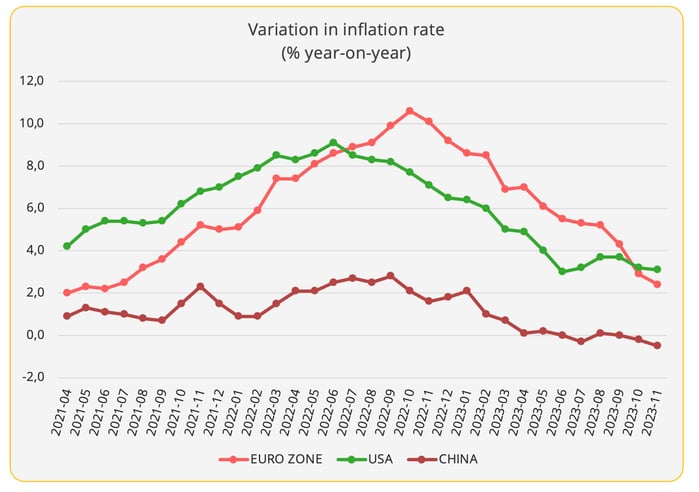

2/ Inflation proved difficult to contain

Sources : Eurostat, US Labour Department, National Bureau of Statistics of China

The drastic policy of monetary tightening carried out by the central banks of the major economies has produced the desired effects. After peaking in the second half of 2022, within a few months of each other, inflation began to decline in both the Eurozone and the United States. In response to this satisfactory trend, the US central bank (The Fed) and the European Central Bank (ECB) have taken a break from raising interest rates.

However, the battle is not yet won. The rate of inflation remains above the 2% target set by these institutions. "We have seen considerable progress on lowering inflation, but inflation remains high and recent readings have been uneven," pointed out Michelle Bowman, a member of the Fed's Board of Governors, at a conference before bankers in Columbus, Ohio on November 7. Indeed, during the summer, inflation rebounded slightly before returning to the downward trend "I continue to expect that we will need to increase the federal funds rate further to bring inflation down to our 2 percent target," stressed Michelle Bowman.

In Europe, in its economic bulletin of October 2023, the ECB estimates that "rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target (of 2%).” But there is no question of loosening its grip until the objective is reached.

"Headline inflation has fallen almost everywhere over the past year, primarily because of the partial reversal of the very large rise in energy prices over the previous two years. However, since June production cuts by key OPEC+ economies have contributed to higher prices. A variety of supply disruptions, alongside rising geopolitical tensions, have also contributed to volatility in European natural gas prices in the latter half of 2023. The upturn in oil prices since June has been reflected in retail prices for petrol, with headline inflation turning back up in some advanced and emerging-market countries," warns the OECD.

In China, the situation is radically different, with almost zero inflation and even deflation observed in July, October and especially in November. Nevertheless, this trend is just as worrying as the overheating observed in Western economies, as it reflects the difficulties facing the Chinese economy, despite the reopening of the country at the end of 2022. “At present, our country’s economic recovery is still at a critical stage,” President Xi Jinping said in a speech delivered at a political rally in Beijing in early December and quoted by the national news agency Xinhua.

Primarily, the country is facing difficulties at the domestic level, including a serious crisis in real estate. On the other hand, in an uncertain economic context, Chinese households maintain high precautionary savings, which is curbing consumption. China states that for 2024, “efforts should be made to expand domestic demand and form a virtuous cycle of mutually promoting consumption and investment”.

The situation is also complex internationally. From a strictly economic perspective, China's post-Covid reopening coincided with a time when Western economies were starting to experience a slowdown, thus limiting the scope of the rebound. On the other hand, politically, the decoupling and "de-risking" strategies vis-à-vis China, advocated respectively by the United States and the European Union, also weigh on its prospects of growth.

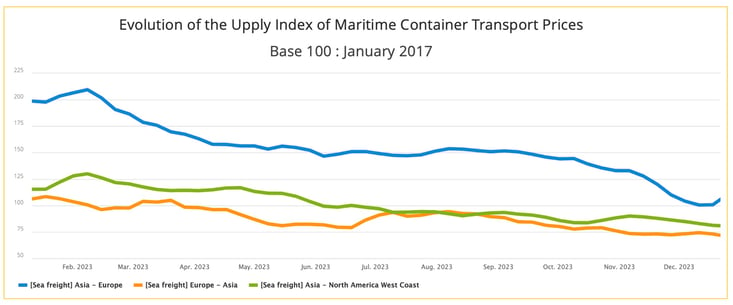

3/ High volatility in transport prices

Inflation continued to weigh heavily on household purchasing power in 2023. The monetary tightening measures adopted to curb the phenomenon have also reduced the investment capacity of individuals and businesses. All these parameters have resulted in a reduction in the demand for goods, and consequently the demand for freight transport.

All modes of transport were affected. But it is in the maritime container shipping sector that price volatility is most dramatic. Freight rates literally soared in 2021, when Covid lockdowns were eased, resulting in a simultaneous influx of orders. On the other hand, the trend began to reverse in July 2022, and continued to the point of seeing freight rates return to pre-Covid levels at the end of the year. The drop in demand coincided with the massive arrival of new vessels, creating a phenomenon of overcapacity that aggravated the supply-demand imbalance and saw freight rates plunge.

That being said, the sector is extremely susceptible to exogenous factors. In December, major shipping companies decided to avoid the Suez Canal and circumnavigate Africa by the Cape ofGood Hope, due to attacks in the Red Sea by Yemeni rebels, the Houthis. Freight rates are thus expected to rise again, at least temporarily and on certain routes such as Asia-Europe, despite the continuation of deliveries of new vessels in 2024.

Source : Upply Freight Index

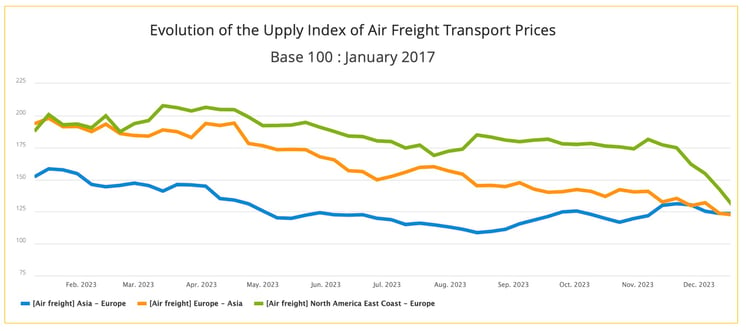

Air freight rates had also jumped in 2021, to a lesser extent than maritime transport. And they are also coming down more gradually. The reintroduction of capacity has been relatively cautious, even if since the spring, cargo supply has increased mechanically, this is due to the increase in passenger flights to meet a demand in full recovery.

Despite a deterioration in the fill rate, air cargo prices remain higher than before the pandemic. 2023's high season remained relatively modest, but still led to a small recovery in freight rates on the Asia-Europe corridor. Demand has proven to be more dynamic in the United States, brightening the outlook for Asia-US flows.

Source : Upply Freight Index

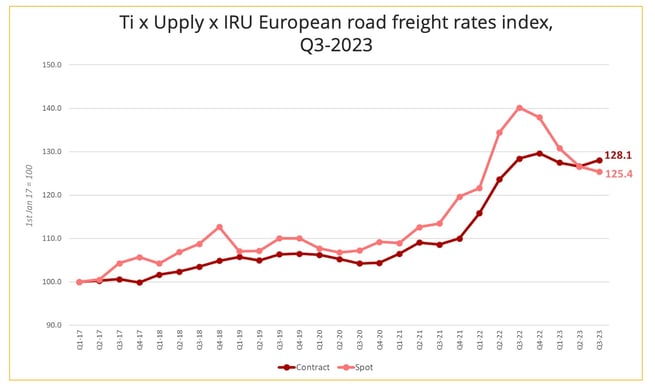

Traditionally less volatile, road freight rates have however joined the general upward trend in 2021-2022 and the downward one in 2023. In this sector, the variation of rates is very closely correlated with that of fuel prices, due to the existence of pass-through mechanisms. This can largely explain the strong resilience seen in contractual freight rates. On the other hand, in the spot market, the "demand" factor dominates, and we can clearly see a strong impact of the decline in volumes to be transported on the European market.

Source : Upply Freight Index

4/ Global trade is facing difficulties

The growth of global merchandise trade is slowing down. "Volumes of traded goods and services are estimated to have grown by only 0.1% at an annualised rate in the first half of 2023, following the weak expansion in the latter half of 2022. Merchandise trade volumes fell by 1.9% annualised in the first half of the year," details the OECD, deeming this increase "surprisingly weak". A pessimism that confirms the updated forecasts of the World Trade Organization published in October. The WTO now expects merchandise trade volume to grow by 0.8% in 2023, down from the 1.7% predicted in its April forecast.

"The trade slowdown appears to be broad-based, involving a large number of countries and a wide array of goods, specifically certain categories of manufactures such as iron and steel, office and telecom equipment, textiles, and clothing. A notable exception is passenger vehicles, sales of which have surged in 2023. The exact causes of the slowdown are not clear, but inflation, high interest rates, US dollar appreciation, and geopolitical tensions are all contributing elements", the WTO report says.The OECD states that data for the third quarter show "some recovery in trade growth in the United States, Japan and Korea, alongside slower, but still positive Chinese trade growth". On the other hand, there has been a contraction in the volume of trade in Germany, France, Spain and the Netherlands.

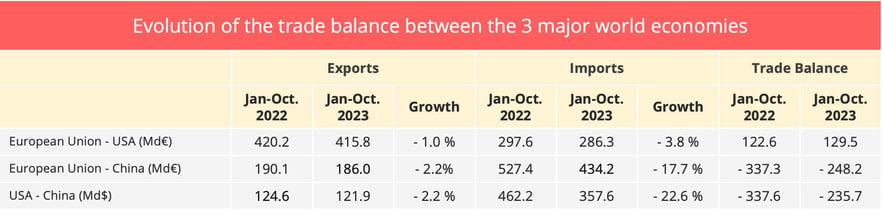

The evolution of the trade balance between the three major world economies in the first 10 months of the year also illustrates the slowdown in trade. Both exports and imports decreased, including a double-digit decline in imports from China to the EU and the United States. The decline is significantly less for transatlantic trade.

Data sources : Eurostat; US Census Bureau

Positive growth in both export and import volumes is expected to resume in 2024 in all regions except the CIS, where imports are expected to decline after 2023’s strong recovery, the WTO estimates, noting that if forecasts for 2024 are confirmed, Asia will be the fastest growing region for both exports and imports. The organization anticipates a 3.3% growth in trade in 2024.

5/ New geopolitical shocks

Start of the China-US trade war in 2018, Covid pandemic in 2020, Russia-Ukraine war in 2022, resurgence of the Israeli-Palestinian conflict in 2023: these crises with lasting consequences, that closely followed one another, have in common had a strong impact on the organisation of logistics chains, through their impact on costs, volumes, production patterns, etc. We could add to these crises extreme weather events that occasionally disrupt supply chains around the world.

It is now clear that more consideration must be given to the weight of geopolitical parameters in the management of supply chains. Western economies, in particular, have become aware of their vulnerability when it comes to accessing certain critical products. At the same time, China is pushing its pawns into position to bring about a new global governance, and is encountering a certain echo, as shown by the expansion of the BRICS announced last August. After decades of primacy given to economics in a system dominated by liberal ideas, politics is back in force around the table. Whether it is to guarantee their security and sovereignty, or to fight against climate change, states find virtues in regulation. Supply chain players will also have to deal with this new situation.