On February 1st, 2019, the EU-Japan economic partnership agreement (EPA) entered into force. This agreement, also known as JEFTA (Japan-EU Free Trade Agreement), creates the largest free trade partnership in the world, with the EU gradually removing 99% of its tariff lines on goods from Japan and Japan removing 97% of theirs on goods from the EU. Can changes already be observed? Let’s look at the first data from the period of February to June.

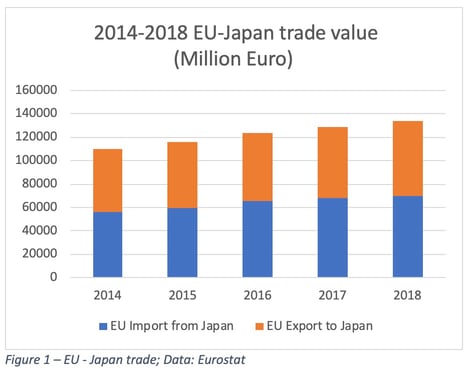

After China, Japan was the EU’s second largest trading partner in Asia, and its 6th largest export destination in 2018. The EU is Japan’s third largest destination for exports, after the U.S and China. The EU and Japan have a relatively even balance of trade, with a slight trade deficit for the EU (Figure 1). The top three product categories that the EU exports to Japan are chemical products, machinery and mechanical appliances, and transport equipment.

This agreement has been dubbed the “cars for cheese” deal by some commentators in the media, as it will gradually remove the Japanese trade barriers imposed on the EU’s agricultural products. Conversely, the EU will gradually remove its 10% tariff on Japanese automobiles over the next seven years. It is estimated by the EU that there will be an annual increase of 13 billion euros of EU exports to Japan and a saving of around 1 billion on duty per year. Other sectors are also expected to benefit from this agreement with a more liberalized Japanese market. For instance, European textile is estimated to experience a 220% growth in exports to Japan.

A significant impact

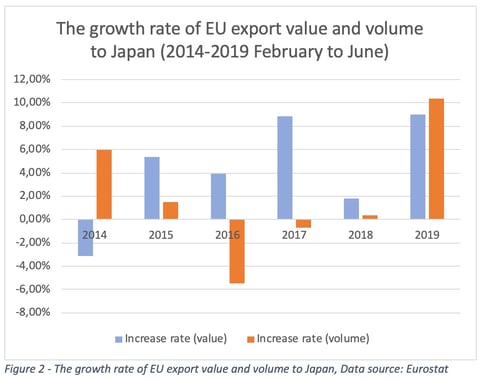

Comparing the period of February to June, 2019, with the same time period over the past five years, the impact of the EPA agreement is significant: The EU’s total exports to Japan reached its highest figure for the last five years, with a 9% increase in shipping value and a 10% growth in shipping volume (Figure 2).

The largest contribution of EU export growth to Japan during this period came from France (see our focus at the end of this article). The increase in French exports accounts for approximately 30% of the total increase of the EU’s exports to Japan over this time period. However, this might not be directly associated with the EU-Japan EPA and may rather be due to Japan Airlines’ purchase of Airbus aircraft in the spring of 2019.

Exports of French wine to Japan also enjoyed a significant increase over the past six months which leads us to take a closer look at the agriculture and food sector.

Focus on agriculture and processed food

So, what about the “cheese” in the “cars for cheese” deal? Access to the Japanese market for EU agriculture and food is one of the focal points in the EU-Japan EPA agreement. According to the agreement, Japan will gradually remove the high tariffs and simplify clearance procedures on EU agricultural products and processed food. For some critical products, the tariff will be greatly reduced, though not fully lifted, over a period of 21 years. With the removal and reduction of tariffs and the implementation of trade facilitation measures, the EPA agreement is expected to enhance the EU agriculture and food industry’s competitiveness in the highly protected Japanese food market. Overall, the positive outcome from February to June is coherent with these expectations, the entire agriculture and food sectors’ exports have increased by 18% in value, which is the highest increase in the past five years, and is up 7% in shipping volume, the peak for the past three years.

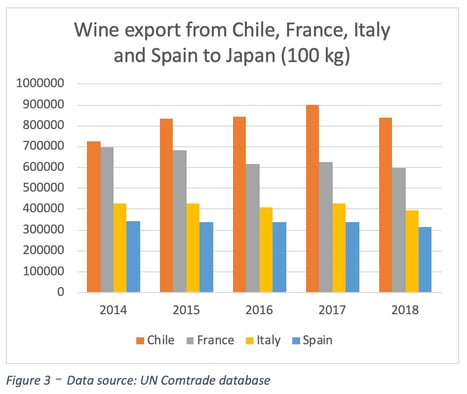

If we take the European wine and spirit industry (HS code 2204) as an example, the 15% tariff was lifted immediately after the EPA entered into force. This allows the EU to better compete with other wine exporting countries, such as Chile, which has a preferential access to the Japanese market. Since the 2015 Japan-Chile Economic Partnership Agreement, the increase of Japanese importation of Chilean wine has been squeezing the market share of wines from EU.

This situation may experience some changes. From February to June, the EU’s export of wine to Japan has surged 23% in value and 25% in volume. The top three EU wine exporters, France, Italy and Spain, have all enjoyed two-digit increases over the past six months (Figure 3).

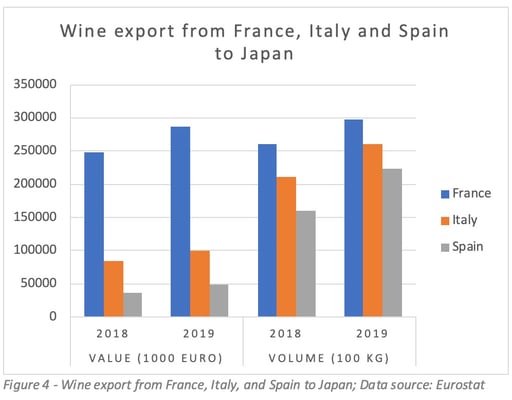

France, as the largest EU exporter of wine to Japan, accounts for over 60% of the export value of EU wine to Japan. Its wine export value increased by 16% and the shipping volume by 15%. Italy enjoyed a 17% increase in value and a 23% increase in volume and Spain enjoyed a 30% increase in both export value and volume (Figure 4).

If we consider other food sectors, where the tariff is only partially removed, are they also enjoying a certain increase in exports following the agreement entering into force? The export value of meat and fish[1], which comes with a long-term gradual tariff reduction, has also surged, with a 7% year-on-year increase for meat and 13% for fish. However, it should be noted that over the past five years, these two sectors have had volatile rate increases. As such, a longer period of observation may be necessary to better identify the pattern of change in exports.

Impact on reefer container shipping market

It has been half a year since the EPA entered into force, and data has brought us a promising picture of EU-Japan trade relations. The crucial question here may be whether this kind of increase can be sustainable, and as such imply a growing demand for shipping capacity on this shipping route.

As the tariff on European agricultural and processed food products will be removed or reduced on a gradual basis over a period of 21 years, a changing demand for reefer container shipping can be envisaged on this route in accordance with the different phases of the tariff removal. Furthermore, with over 200 European agricultural products with a “Geographical Indication” certification being recognized in the Japanese market, only products with this status would be allowed to be sold in Japan under the corresponding name. This also contributes to the EU’s competitiveness in the Japanese food market.

Furthermore, with the gradual removal of tariffs and trade facilitation measures, this means more varieties of European agricultural and food products can enter the Japanese market than ever before. This may result in a growing demand for the technology and shipping safety of reefer containers in order to meet the needs of diverse food and agricultural products.

The EU-Japan EPA agreement sets an admirable example of free trade under the current wave of trade protectionism. Of course, long-term sustainable growth will only come with continuous implementation from both sides. However, we must take into account the progress in U.S-Japan trade negotiations, which will mean that EU agricultural and food sectors will possibly face stiff competition from US agricultural products in the future.

[1] Here I use the trade data of HS chapter 2 and chapter 3, which includes the meat (chapter 2) and fish (chapter 3).

Photo : @ Anne Kerriou