The world economy should return to growth in 2021, with the rate of growth estimated at 4% to 5.5%. International trade in goods and services, on the other hand, could grow by 8.1%.

In 2020, the world faced its fourth deepest recession in 150 years. According to World Bank estimates, the economic measures taken to halt the spread of the coronavirus epidemic caused a 4.3% fall in global GDP.

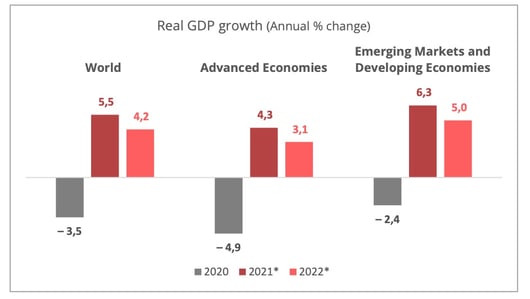

The epidemic is not yet over but the economic outlook is getting brighter. The World Bank is forecasting that the global economy will grow 4% in 2021 and 3.8% in 2022. The IMF is even more optimistic, forecasting 5.5% growth in 2021 after a 3.8% reduction in global GDP in 2020.

The emergence of the world economy from recession will, however, be more than ever marked by major regional disparities. Emerging countries are expected to achieve a high 6.3% growth rate, while developed countries can expect more moderate 4.3% growth.

Source: IMF, Upply (* forecast)

China, the country from which the virus originated, comes out the winner with growth of 2.3% in 2020. Latest statistics confirm that the country is experiencing a V-shaped recovery, driven by manufacturing and high export levels. Growth is expected to attain 8.1% in 2021 and China's GDP looks to be well on the road to overtaking that of the United States by 2028.

The forecasts of the Organisation for Economic Cooperation and Development (OECD) are close to those of the World Bank. They predict a return to global growth in the third quarter of 2021, with growth expected to reach 4.2% in 2021 and 3.7% in 2022. The organisation's least optimistic scenario, which takes account of possible disappointments regarding vaccine distribution and side-effects, suggests that the return to global growth could be delayed by 12 months.

Despite these slight divergences, the international organisations all increased their estimates in 2020 and are unanimous in predicting strong global growth in 2021 despite major uncertainties.

Unprecedented economic support

After a year of the health crisis, states and central banks have steadily expanded their support programmes for companies and vulnerable population groups. These programmes have enabled economic activity to be preserved and the most vulnerable population groups to be protected. Direct aid and loan support have prevented many companies from going under. According to IMF analysis covering 13 advanced countries, the number of company failures has been lower than in any previous recessions since 1990.

In the United States, the new Biden administration has put forward a $1,900 billion plan, which comes in addition to the $900 billion Trump plan adopted in December. The new support plan, if it is adopted, will account for nearly 10% of American GDP and will quickly boost American consumption.

European leaders approved an economic recovery plan with funding totalling €750 million and a pluri-annual budget totalling €1,074 billion over the seven-year period from 2021 to 2027. For the first time, the European Union will take on debt to be able to grant the loans and subsidies required by its member countries. The main advantage offered by these 30-year loans is their repayment mechanism. They will be financed by new taxes on access to the EU market. Their exact form has not yet been totally decided but it would seem that the EU is moving towards imposition of a carbon border adjustment tax and a digital economy tax. The EU's problem is to find a way to avoid saddling itself with a debt level which is unsustainable in the longer term.

Resilient leading indicators

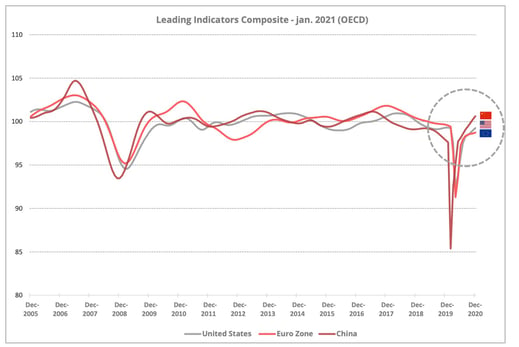

Assuming there is no new wave of the epidemic, the outlook should improve in the second quarter of 2021. According to the IMF, international trade in goods and services can be expected to grow by 8.1% in 2021 and by 6.3% in 2022. The OECD's composite leading indicators are already showing major return to growth in developed economies.

- The Chinese economy is even showing signs of a return to pre-crisis growth levels, driven by industry, exports of personal protection equipment and the semi-conductor sector. The leading indicators for 2021 are clearly in positive growth territory.

- In the United States, prospects are improving with an unemployment rate of 5% in 2021 and 4.2% in 2022, compared to 6.7% in 2020, according to the American Federal Reserve. The reduction in unemployment has been massive since the 14.8% high recorded in April 2020. Another tell-tale sign has come from the construction industry. New construction site starts increased by 6.3% in December 2020, representing 1,669 million new homes - the highest total for 14 years. The new administration's 2021 recovery plan is still being prepared.

- In Europe, first half activity is likely to be very dependent on the prevalence of restrictions imposed as part of the battle against Covid-19. In January 2021, only Germany produced a positive business activity result in the manufacturing and services sector purchasing managers' index. Projections for the automobile sector in 2021 are nevertheless positive, with a 10% increase expected in new vehicle sales, according to the European Automobile Manufacturers' Association.

Some sectors are nevertheless in a state of extreme weakness, particularly the hotel, restaurant and leisure industries. The International Road Transport Union has also raised the alarm over the liquidity shortage in the road transport sector following the sharp drop in freight volumes it suffered in 2020. A boomerang effect cannot be excluded in 2021, therefore, if aid starts to dwindle.

Three scenarios for 2021

- The economic situation worsens in the first half as a new wave of the epidemic gets under way and a new variant of the virus emerges which governments struggle to contain. This would lead to an alarming loss of business confidence and a tightening of credit terms, with the risk of an increase in company failures and states unable to increase their debt ratios.

- The economy moves quickly into a V-shaped recovery in the second half, boosted by efficient vaccine distribution, clear progress in available treatments or a natural weakening of the virus. In this case, consumption will be extremely dynamic and economic growth will be similar to what it was in the third quarter of 2020 (33.4% in the United States, 12.5% in Europe).

- The economic situation recovers gradually but unevenly, according to the fundamentals in the different economic sectors, the different geographical zones and investment stimulation measures. In this case, growth, driven by investment, would follow a longer cycle of nearly 18 months and could generate distortions in competitiveness, followed by radical changes in the economic environment.

The macro-economic fundamentals also highlight the risk of a sharp increase in raw material prices in 2021. The recent signing of a free trade agreement between Asian and Pacific countries could accentuate this trend by boosting recovery. The output of the countries which signed the agreement is heavily dependent on mineral and energy resources. Oil prices, too, could come under heavy pressure as the economy recovers and people become mobile again in the second half. According to the latest information from the financial markets, an increase in the price of crude oil of about 20% can be expected in 2021.

The world economic landscape will probably begin a process of profound transformation. The disorganisation suffered by supply chains in 2020, particularly in the health sector, has engendered a real awareness of the need for countries to be self-sufficient in certain key sectors. We could, therefore, see some sort of reindustrialisation, coupled with a drive to limit the ecological impact of production processes. This trend should get strong support from governments, as well as being encourage by the development of "green financing". The European Union has already given notice, moreover, that recovery measures must lead to a "greener, more digital, more resilient" Europe.