The coronavirus crisis with its generalized and planetary lockdown measures has generated the deepest recession since World War II. Signs of recovery are appearing, even if the forecasts made by international organizations remain pessimistic. Ultimately though, this crisis could be a tremendous accelerator for innovation and change in supply chains.

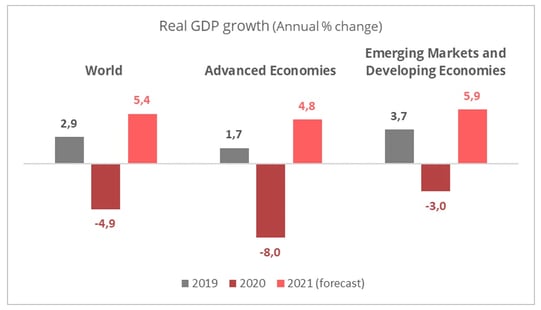

The latest World Bank forecasts estimate that the measures taken to stem the coronavirus epidemic by halting activity will cause a 5.2% drop in global GDP in 2020, followed by a rebound of 4.2% in 2021. For its part, the IMF is a little more optimistic estimating a 4.9% decline in global GDP for 2020, but with considerable regional disparities. Developed countries will be the hardest hit with a drop of 8%, while emerging countries will suffer a more moderate impact of a drop of 3%.

Source : IMF, Upply

The Organization for Economic Co-operation and Development (OECD), for its part, is more pessimistic. A first scenario estimates the decline in global growth of 6% in 2020, with a rebound of 5.2% for 2021. The analysis is based on the “single-hit” scenario, that is to say the current phase of Covid-19, associated with a restart of economic activity and the absence of a 2nd epidemic outbreak, followed by a phase of sustainable economic recovery combined with a treatment or a vaccine. A less optimistic scenario is based on a 2nd epidemic outbreak whose consequences are more uncertain, with a risk of recession of 7.6% for the global economy in 2020 and then a growth of 2.8% in 2021.

Despite these slight disparities, international organizations unanimously evoke a strong global growth forecast for the year 2021. However, it will take at least another year before a return to 2019's levels is achieved.

Major support plans

All the world's economies suffered a shock of unprecedented magnitude in the 1st half of 2020, but the support and recovery plans from European and American governments clearly met the needs of economic actors, even if improvements to these plans are still possible in some sectors. EU leaders have agreed to an economic recovery plan funded at 750 billion euros and a common multi-annual EU budget of 1,074 billion euros over seven years (2021-2027). Faced with an unprecedented crisis, Europe has provided an innovative response. For the first time ever, the Commission will borrow on behalf of the European Union and then allocate the necessary loans and grants to member countries.

The US government has also implemented a massive $ 2 trillion stimulus plan of unemployment support and business loans. In addition, a new plan of 1,000 billion dollars is being prepared for cities and school districts but also especially for small and medium-sized companies which employ nearly half of all private sector workers and represent nearly 44% of the American GDP.

Positive indicators

The US economy is showing some signs of buoyancy with a revival of manufacturing production. Monthly surveys of US purchasing managers (PMI) show a 19-month high with a figure of 53.6 for the month of August. For the European economy, this same indicator stands at 55.7 which is its highest value for 28 months.

On the other hand, Upply's data on freight prices for French sea, air and road modes shows that with the resumption of activity over the summer comes an increase in prices.

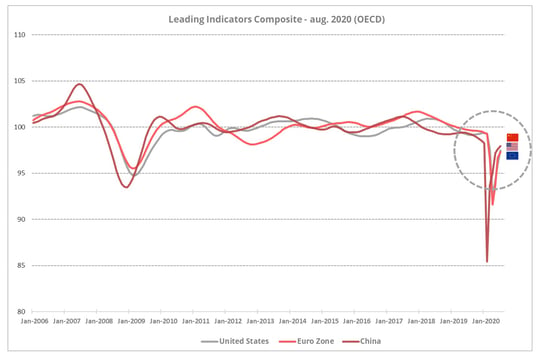

Furthermore, Composite Leading Indicators calculated by the OECD show a significant resurgence of growth in developed economies. The situation in China is even showing signs of a return to pre-crisis levels. Nevertheless, the second half of the year will continue to be dependent on the evolution of the global health crisis and the potential risk of a second wave.

Source: OECD, Upply

Three post-vacation scenarios

Several hypotheses are on the horizon for the beginning of the last quarter of the year.

- The economic situation worsens with a second wave of the epidemic, which governments will have difficulty in containing this time, which provokes serious societal consequences, redundancy plans and a stock market value correction

- The economic situation recovers rapidly in a V shape curve and cases of contamination no longer lead to death given the conclusive progress in available treatments

- The economic situation adopts a gradual but asymmetric pace of recovery which will be highly dependent on the essential characteristics of each economic sector.

The last quarter of 2020 will be decisive because the entire impact of lockdown measures will then be integrated into company accounts and a significant increase in the number of companies going into payment default or bankruptcy will be expected. However leading economic indicators, dynamic production and consumer confidence levels show that an economic recovery should overcome the fear generated by the health risk. A rebound can be expected in 2021, based on a scenario of gradual and asymmetric recovery. In a number of sectors, the consequences of the total shut-down of certain territories will take several more quarters to dissipate, for example in the hotel and automotive industries, or even several years in the case of the aeronautics sector. The International Air Transport Association (IATA) estimates that the global shortfall for the sector $419 billion and that a return to the normal pre-crisis situation will not be not possible before 2024.

Whatever the outcome, economic development remains uncertain. To face potential risks, preserving the income of a company requires diversified management of its supply chain which, when combined with protection provided by financial mechanisms, can mitigate the risk of volatility.

This type of extreme situation is also an accelerator for economic change. Market players are more likely to adhere to innovative products and companies are positioning themselves in new markets. Innovation, digital solutions, and operational resilience of supply chains will guarantee a long-term operating margin.