The Chinese economy, which is the great driver of global growth, is showing signs of slowing, as the pandemic is continuing to disrupt supply chains. As a result, the shipping companies are having to navigate from point to point.

It is always helpful to reflect on the journey we have made to understand where we are heading…As we have regularly pointed out in our market analysis articles over the last two years, the huge volume of merchandise which needed to be got out of China urgently after the first Chinese lockdown in March 2020 created the inflationary conditions which still prevail in the container shipping market between Asia and the West.

In 2021, the consumer catch-up caused an overheating of demand which, apart from a few calmer periods, never really faltered until February 2022. March, however, was marked by a slowdown which has raised questions over the direction the market is likely to take in the short term.

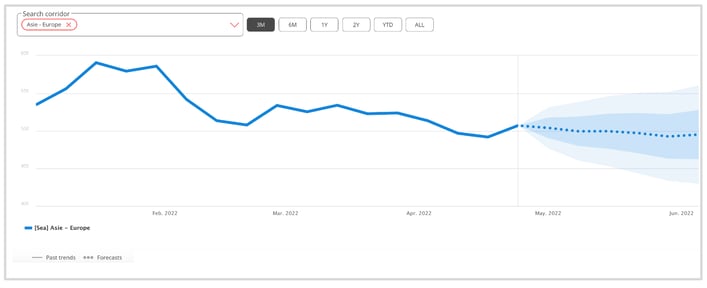

1/ Asia-West freight rates stay high

Will they come down or not ? That is the big question facing the market in this early spring period regarding Asia-Europe freight rates.

We understand better now why the big shipping companies were in such a hurry to sign as many long-term contracts at high rates as they could during the winter season. "Carrier discipline" is clearly militating in favour of maintaining high rates rather than high cargo volumes. The slight reduction currently being seen in Chinese export rates is clearly not commensurate with the fall in cargo volumes currently available.

The Asia-Europe freight rate trend over the last three months and prospects for the six months to come - Source : Trends, Upply SMART

The shipping companies are counting on a recovery in Western demand in May-June after the intermediate period of lower demand we are currently going through, during which they need to keep freight rates high. This "bridging" strategy will be particularly uncertain and risky, however, if Western demand remains soft until the end of the spring or the start of summer.

2/ China still needed to drive demand

In the absence of credible alternatives, China is still indispensable to the global economy and the container shipping industry, which needs its huge export flows to fill its giant container carriers.

Today, however, there is a great deal of uncertainty regarding its future. China is battling to beat the pandemic via a "zero Covid" strategy, which is taking a heavy toll on its economy. As cases of infection increase again, massive population lockdowns were imposed in major urban centres in April. Little by little, production is slowing, with a detrimental effect on supply chains which are already in poor shape. Ports and airports are still open but are operating at reduced capacity, while, in the road transport sector, chaos reigns.

For the shipping companies, all this means a loss of cargo volume in the short term. China's Asian satellites, Vietnam, Indonesia, Thailand, Japan and Korea, are able to partly make up the shortfall, which is what they are doing, but the cargo they are able to generate bears no comparison to the reduction in Chinese output. As regards the level of freight rates, the shipping companies can hope that the same causes will produce the same effects and that, when the disruption eases, we will see a sharp recovery in demand, as we did in 2020, which will help to keep freight rates at a high level.

A certain number of unfavourable signals have made an appearance, however. China has set itself a growth target of 5.5% in 2022, which would be its lowest growth rate for 30 years. If the Chinese economy continues to under-perform in the long term, there is a real threat, even if will not become reality from one day to the next.

The West's heavy reliance on China has been clearly felt and documented for a number of years but it was only when the pandemic arrived that Western leaders began to consider it a serious strategic consideration. The idea that we should make a virtue of consuming less, with less long-distance transport and an effort to reduce distances between production sites and places of consumption, has wide support. It remains to be seen, however, if this is a luxury that the West can afford, since, even with transport costs at a high level, Asian goods are still being offered at unbeatable prices. Now that inflation is taking off again, this question has become even more pressing.

From the environmental point of view, we often forget that reindustrialisation has a corollary in terms of energy consumption. Strangely, industrial pollution is not seen in the same way when it is caused a long way away rather than under our own noses. Of course, the West is highlighting its plans to create industries with a much reduced carbon footprint but these plans will take years and even decades to realise rather than months. German industry, which, in the light of the war in Ukraine, we now see as excessively dependent on Russian gas, is a clear example. Even if Europe wanted to reindustrialise quickly on a grand scale, it simply does not the energy to do it.

The energy question is less critical in North America. Where purchasing power is concerned, however, the situation is the same on both sides of the Atlantic. In other words, the health of the Chinese economy has become a decisive factor for that of the global economy…and that of the shipping companies.

3 / Are the shipping companies worried ?

After decades of starvation rations, the shipping companies clearly intend to enjoy the opulence they have known over the last 18 months for as long as possible. For them, therefore, the current shipping cycle should be made to last as long as possible, helped if necessary by maximum capacity restrictions. At the port of Antwerp, container throughput declined by 11.6% year-on-year in the first quarter of 2022. "The disruption to container liner trade, delays and high import call sizes (number of containers unloaded by ships) are posing protracted operational challenges, which are making the operation of the container terminals more difficult," the port said in a press release. "Moreover, the Russia-Ukraine conflict and the sanctions imposed also put pressure on the number of containers handled.".

The shipping companies have three main fears :

- that Western inflation could get out of control, causing a long term drop in demand from households and companies;

- that uncertainties regarding the Russia-Ukraine conflict could become a long-term phenomenon, creating the risk of a contagion that could increase by the day;

- that the market could be "punished" in the event that there is a reversal of the relationship between supply and demand. This last fear, which is the most "psychological "of the three, is, strangely, one which comes up frequently in the casual exchanges one can have at the moment with the shipping companies' commercial and marketing departments.

Paradoxically, therefore, the shipping companies are not feeling totally reassured despite their record profits. They have been traumatised by the painful memory left by their years of great financial weakness and are ready to impose stricter discipline to keep control of the situation. Clearly, the market is uncertain about the behaviour of fundamentals in the months to come. What they can take now cannot be taken back but, two years after the start of the pandemic, the shipping companies are still having to navigate from point to point.