The slowdown in global growth is expected to worsen in 2023. A trend that will reflect on the trajectory of international merchandise trade whose growth will fall below 2%. Soaring transport prices are over.

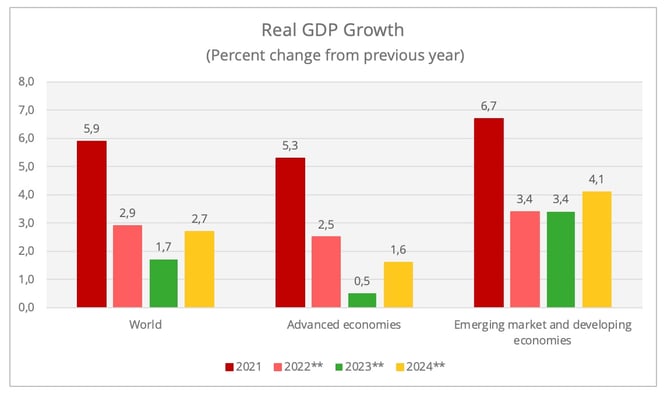

In 2022, all of the world's major economies were hit by a slowdown, after the rebound of 2021. According to World Bank data, the growth rate of real gross domestic product fell from +5.9% to +2.9% for the world as a whole. In advanced economies as well as in emerging markets and developing economies, the pace of economic growth has thus been roughly halved, disrupted by “elevated inflation, higher interest rates, reduced investment, and disruptions caused by Russia’s invasion of Ukraine.”

Rather bleak forecasts for 2023

The slowdown will continue and even worsen in 2023, estimates the World Bank. The institution has drastically revised its forecasts downwards as it puts forward a GDP growth rate of +1.7% on a global scale for 2023 in its updated forecasts in January, against a much more optimistic estimate of +3% announced during the previous forecast published in June 2022. The World Bank drove the point home in its report, stating: "The sharp downturn in growth is expected to be widespread, with forecasts in 2023 revised down for 95% of advanced economies and nearly 70% of emerging market and developing economies". It went on to say: "Given fragile economic conditions, any new adverse development—such as higher-than-expected inflation, abrupt rises in interest rates to contain it, a resurgence of the COVID-19 pandemic, or escalating geopolitical tensions—could push the global economy into recession. This would mark the first time in more than 80 years that two global recessions have occurred within the same decade."

*Estimate; **Forecast – Data source: World Bank

While the trajectories between advanced and developing economies have run more or less parallel over the past two years, the continued slowdown is expected to hit advanced economies much more sharply, with GDP growth estimated at only 0.5% in 2023. The World Bank forecasts growth of 1% in Japan, 0.5% in the United States, and stagnation in the Eurozone.

Emerging markets and developing economies, on the other hand, are expected to maintain the same growth rate as in 2022 (+3.4%, 0.8 percentage points lower than the World Bank forecast in June 2022). This increase will be clearly bolstered by the South Asia and East Asia/Pacific zones, which are expected to register increases of +5.5% and +4.3% respectively. The former will benefit from the favourable dynamics observed in India and Bangladesh, while the latter will be able to capitalise on a rebound in the Chinese economy and driving winds from Indonesia. However, in the immediate future, China continues to face new outbreaks of COVID-19 and production disruptions associated with weak external demand.

**Forecast – Data Source : World Bank

The International Monetary Fund and the OECD are less alarmist in their 2023 forecasts. The OECD forecasts global growth of 2.2% in 2023 and 2.7% in 2024.

As for the IMF, it slightly revised its October forecast upwards, with growth estimated at 2.9% for 2023 and 3.1% for 2024. The assumption is, +1.2% for advanced countries, and +4% for emerging and developing countries.

In the euro zone, the situation remains very fragile, especially for the largest European economy, Germany, which is expected to stagnate. Spain, on the other hand, is close to the European average with +1.1%, against +0.6% for Italy and +0.7% for France. This latest forecast is significantly higher than the figure of +0.3% put forward by the Banque de France. More bad news for the European economy: the UK, which remains a key trading partner for the EU, is expected to experience a recession of -0.6%. It is the only major global economy for which the IMF is forecasting a recession.

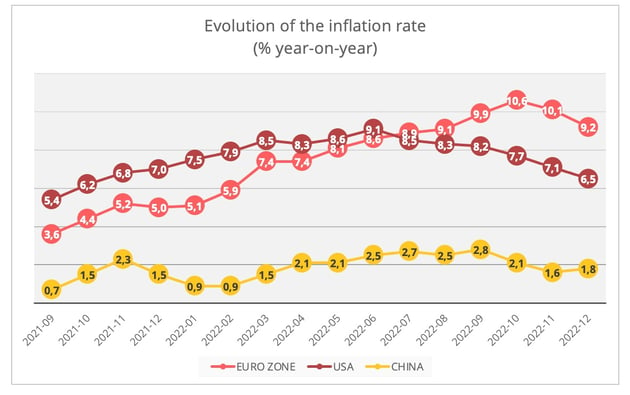

Inflation is falling but remains high

The parameters that will drive global growth downward are the same as in 2022: “The forecast of low growth in 2023 reflects the rise in central bank rates to fight inflation, especially in advanced economies, as well as the war in Ukraine,” the IMF said. Thus, in the latest revision of its forecasts, the IMF took into account global interest rates revised upwards, “reflecting intensified actual and signaled policy tightening by major central banks since October”.

This policy of fighting inflation is beginning to bear fruit, with a decline in it observed since July in the United States and since November in the Euro Zone, while China remains relatively unaffected by this trend. However, in OECD countries, inflation will remain above the 5% mark in 2023.

Upply - data source: Eurostat, US Labour Department, National Bureau of Statistics of China

Inflation will therefore have a lasting impact on household purchasing power, but also on the operating costs of businesses, which are suffering in particular from the increase in energy and raw material prices. According to the IMF, in 2023, oil prices are expected to fall by about 16%, while non-fuel commodity prices are expected to fall by an average of 6.3%.

Decline in world trade

The general economic environment is strongly affecting world trade, whose growth, after falling to 4% in 2022, is expected to slow even further to 1.6% in 2023, according to World Bank estimates. Trade in goods, in particular, is expected to dwindle due to weak demand and a gradual shift in consumption towards services.

The World Trade Organisation confirms this diagnosis. WTO economists, in their forecasts published in October 2022, have estimated the growth of the volume of global merchandise trade at only 1% for 2023. This is a very sharp decline from the +3.5% in 2022 and the previous estimate of +3.4% for 2023.

Source : WTO

The WTO, however, insists that “there is a high degree of uncertainty associated with the forecast due to shifting monetary policy in advanced economies and the unpredictable nature of the Russia-Ukraine war.” The WTO forecasts suggest a low hypothesis of -2.8% “if the downside risks materialize” and a high hypothesis of +4.6% if “surprises are on the upside”.

Lull in transport prices

While inflation is far from being contained, there is one area where costs are falling sharply for businesses: transport and logistics. The end of the vigorous post-Covid recovery movement, which had disrupted supply chains, has helped reduce difficulties in access to transport capacity and in infrastructure congestion.

In containerised shipping, in the flagship markets of Asia-Europe, freight rates are almost back to pre-pandemic levels after being multiplied by 5 at the height of the overheating period. In air freight, prices are also contracting, even if they remain rather higher than in 2019. These two sectors have been hit hard by the slowdown in trade, to the point that the traditional “high season” that usually precedes Christmas and the Chinese New Year has not been palpable this year.

The road transport sector generally reacts with a lag of a few months compared to international transport. This was again the case during this crisis. According to the Upply/Ti/IRU European Road Freight Rate Benchmark, freight rates reached peaks during the 3rd quarter. On the other hand, in the 4th quarter, the index showed a decline, both in the spot market and in the contract market.

The year 2023 therefore promises to be a tricky one for transport operators, who will have to manage this fall in rates while their operating costs are still very much affected by inflationary pressures, particularly in terms of energy prices. For shippers, lower rates are good news...up to a point. The fragility of service providers also brings its share of uncertainties. After allocating massive aid to prevent their economies from collapsing during the Covid-19 pandemic, states are all the more eager to end support measures as rising interest rates deepen debt.

When the supply chain dances on the edge of a precipice

Over the past three years, the unthinkable (or unthought-of) has entered the world economy, first with the Covid-19 pandemic and then, despite the ongoing first event, the return of war in Europe.

These two events have disrupted the daily lives of transport and logistics professionals, who have had to adapte urgently to ensure the continuity of the business. In the longer term, they mark the emergence of geopolitical factors and their hazards at the heart of the supply chain. The Allianz Risk Barometer 2023 is starting to reflect this trend, with the notion of “political risks and violence” now in the Top 10 (while the pandemic risk has disappeared from it). However, it is not certain that companies have yet fully grasped the extent of the upheaval that this implies for the strategy of globalisation as we have known it for three decades.

Source : Allianz Risk Barometer 2023

Rehabilitated by the shortages that made the Western world understand its excessive dependence on distant and/or potentially hostile suppliers, the notion of economic sovereignty returned to the forefront with the Covid-19 pandemic and found itself reinforced by the outbreak of war between Russia and Ukraine. It has far-reaching consequences in terms of world trade. The United States has drawn up an "Inflation Reduction Act", which is a law introducing very protectionist measures quite incompatible with their announced intention to promote "friend-shoring". The European Union responded on 1st February 2023 with its "Green Deal Industrial Plan". "An underappreciated risk would be the decoupling of major economies from global supply chains. This would exacerbate supply shortages in the near term and reduce productivity over the longer term." says the World Trade Organization.

In the shorter term, the barometer of risks specifically identified in the transport & logistics sector, published for the first time by Allianz, sums up quite nicely the roadmap that awaits professionals in 2023! The economic environment remains of course the main concern, but there is also a particular sensitivity to legislative and regulatory developments. The energy crisis, which is very prevalent in the sector, is also forcing itself into the Top 5 on a par with cyber risk, while the threat of business interruptions is receding.

Source : Allianz Risk Barometer 2023

Contrary to what is sometimes heard, globalisation is not a thing of the past. It is a lasting and structuring foundation of the global economy. On the other hand, the patterns of globalisation conceived in the 1990s have revealed their limits, their vulnerability and consequently their obsolescence. 2023 has started under stormy economic skies, which could brighten in the second half of the year. The skill of transport and logistics professionals will be measured by their ability to manage the activity in the short term in this complicated context, while investing or at least preserving the ability to invest in order to face the growing structural challenges, from the energy transition to digitalisation through to the reconfiguration of value chains. We have seen shipping companies put themselves in order of battle thanks to replenished treasury levels. Major new operations in the freight forwarding sector can be expected.