The European Union and the United States have each published reports on the robustness of their supply chains and ways to address their vulnerabilities. We offer a comparative review of their analyses.

In both Europe and the United States, the Covid-19 pandemic has highlighted the strategic importance of supply chains, drawing attention to the need for public policy changes to ensure better supply chain security. In May and June, within weeks of each other, the EU and the US each published a review of their supply chains, identifying the bottlenecks, and the policy tool kits to address these vulnerabilities. This article makes a comparative review of these two documents and discusses the dynamics they may bring to the global supply chain.

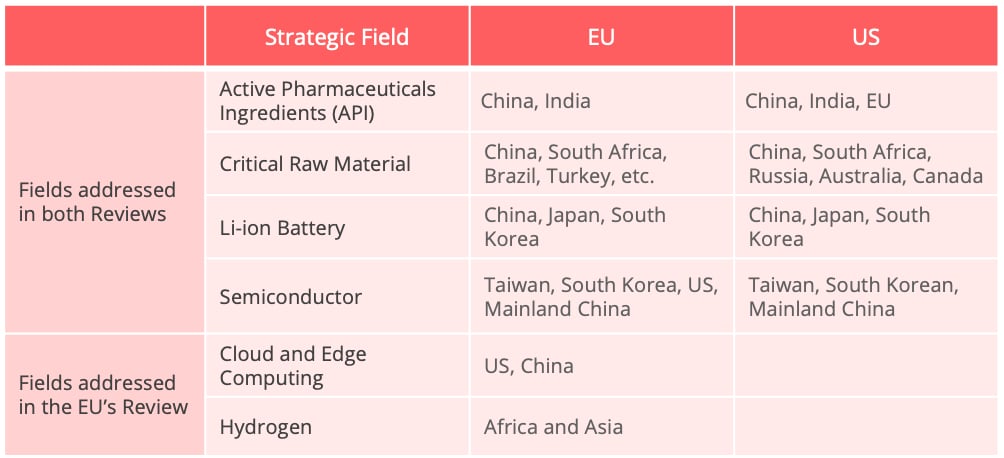

Strategic Fields Identified

The EU and the US have both identified raw material, electric vehicle batteries, semiconductors, and the pharmaceutical industry as being strategic sectors with vulnerable supply chains. Hydrogen and cloud computing are also considered as critical sectors in the EU’s supply chain review.

The key weakness as laid out in both reports is the highly concentrated reliance on a small number of suppliers in these sectors (Table 1). In the EU case, 6% of the imported sensitive goods are highly reliant on imports from third countries. The top three countries that the EU is dependent on are China (52%), Vietnam (11%), and Brazil (5%) (1). The US report highlights the heavy reliance on supply from China and its market.

Table 1- Strategic Fields and dependency identified by the EU and the US in their Supply Chain reviews. Summary by the author based on both Reviews.

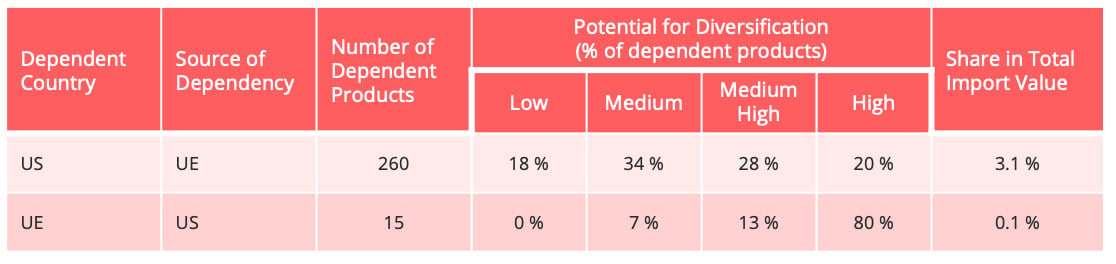

Furthermore, the EU and the US are also interdependent on the supply of APIs, raw materials, and electric generators, though asymmetrically (2). Overall, the EU is less dependent on exports from the US than vice versa (Table 2).

Table 2- The Strategic Interdependency between the US and the EU. Data Source: Strategic Dependencies and Capacities, European Commission.

Policy Tool kits

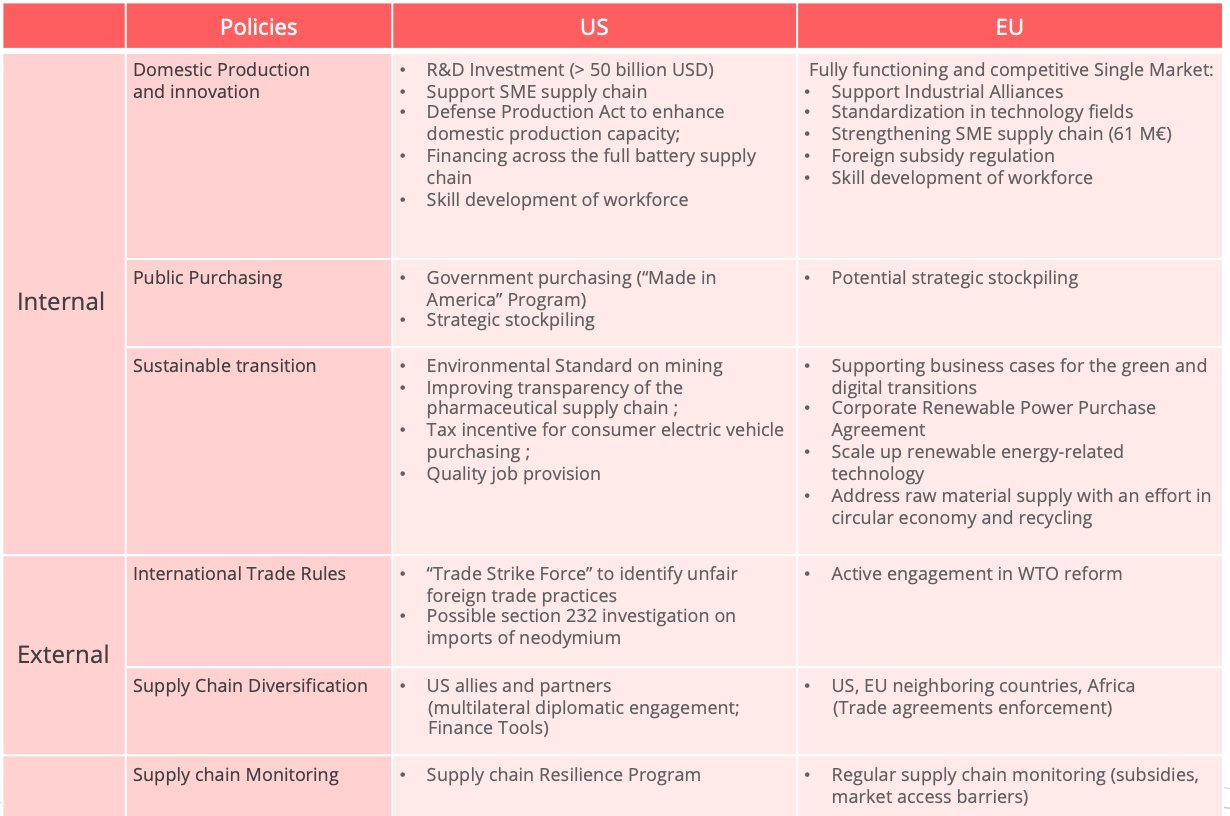

Both reports presented a series of policy tools to address the various vulnerabilities in the supply chain. Twenty-three recommendations for six categories are included in the US report. The EU policy tools address digital and sustainable transition, single market reform, and rule-based international trade (Table 3). Some recommendations cover several issues. For instance, the EU hopes to increase the internal critical raw material supply through a circular economy approach.

In short, the EU and the US adopt similar approaches to address supply chain vulnerabilities: strengthening internal supply capabilities and externally by diversifying sources of supply and export markets. Of course, the boundary between internal and external is blurred in actual implementation. For example, shaping global standardization in strategic fields, as one of the EU’s tools to secure its competitiveness, requires coordination within the single market and with external actors.

As for trade policy, both the EU and the US emphasize building rule-based international trade and strengthening the economic connection with like-minded countries and neighboring countries. Yet, there is a nuanced difference. The EU places a greater emphasis on securing a level-playing field for the EU in the global market, while the US stresses more on strategic competition with China. These different policy objectives could lead to the implementation of divergent policies in practice, despite common interests.

Table 3 - Comparison of the Policy Tool kits - Data Source: information generated from EU and US Supply Chain Reviews, EU and US Trade Policy Review, and EU industrial strategy. Noted: This is for illustration purpose, not all the policy tools are included.

The impact of the new Supply Chain Dynamics

A critical question here is what can we anticipate following the growing engagement in policies addressing supply chain security? Let us elaborate on three likely tendencies.

- Revival of Transatlantic Trade

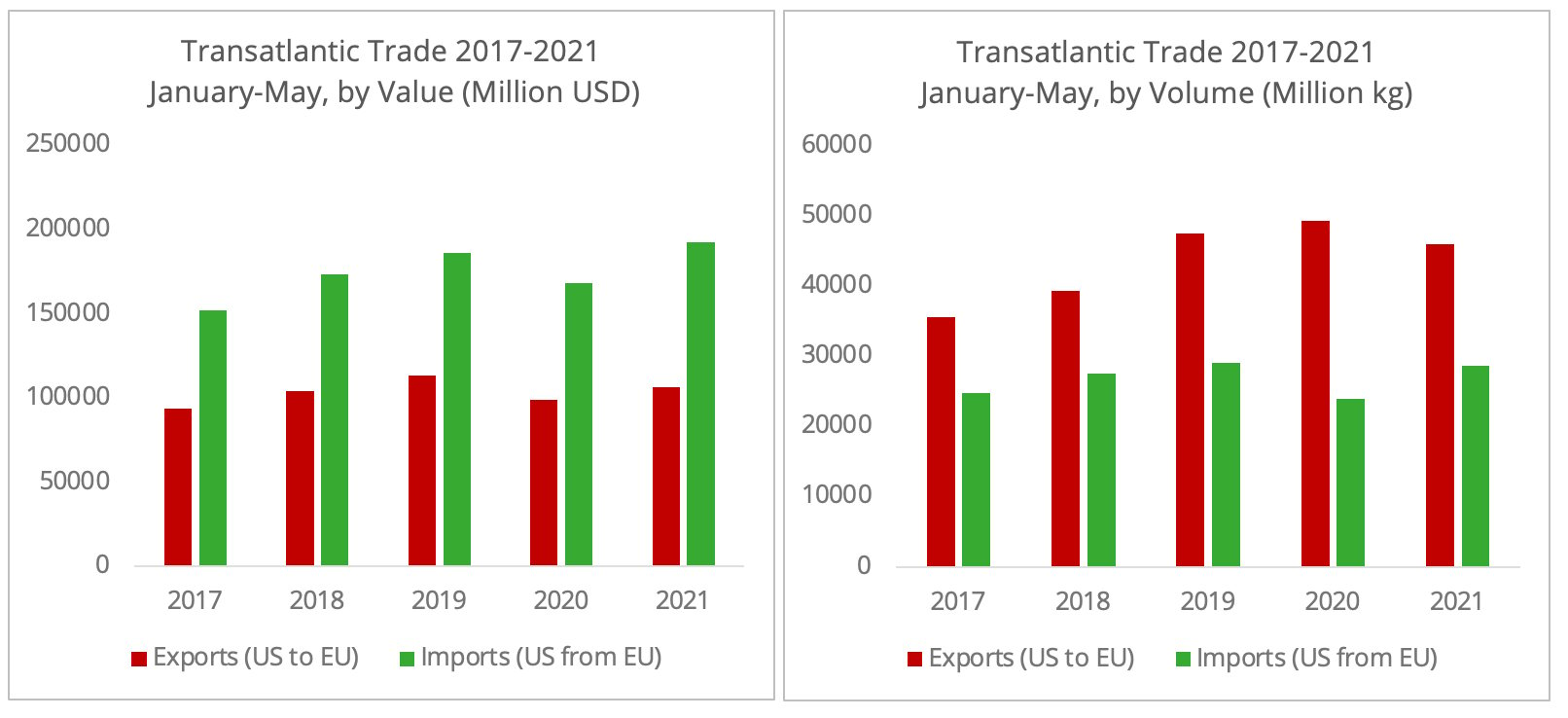

The shared interest and strategies between the US and the EU in addressing their supply chain vulnerabilities undoubtedly contribute to the revival of transatlantic trade.

In the short term, the suspension of additional tariffs and the economic recovery from the pandemic is likely to reboot the bilateral trade. The first five months of 2021 marked the highest record for US imports from the EU for the same period over the past five years by value (Figure 1).

Figure 1- Data source: US Census Bureau

The recent suspension of additional tariffs due to transatlantic trade disputes (3) will benefit the bilateral agriculture and food trade, especially for alcoholic drinks, one of the hardest-hit sectors. The timing is also perfect: the summer vacations and the gradual lifting of a number of restrictions on social distancing are conducive to a greater demand for alcoholic beverages and gourmet food.

Long-term bilateral relations will depend on the progress of the transatlantic trade deal. Indeed, this trade deal is of mutual interest. However, to what extent can common ground be found between "Made in America" and the EU's "Open Strategic Autonomy"?

It is likely that we will observe growing transatlantic trade in strategic sectors. In particular, the EU is likely to increase its purchases from the US in certain strategic fields driven by political motives. For instance, the EU’s imports of US soybean from the 2018-2019 crop year drastically increased by 121% after China stopped purchasing US soybean. A move that followed a meeting between former European Commission President Jean-Claude Junker and U.S. President Donald Trump in a bid to avoid additional tariffs on the EU automotive industry. The EU imports of US soybean from the 2020-2021 crop year declined 46% in comparison with the 2018-2019 season, following the recovery of Chinese demand.

These "political" efforts are not necessarily negative from an economic point of view. For instance, the EU managed to import US soybean, an agricultural product that the EU largely relies on imports for, with a reduced price due to the withdrawal of Chinese demand.

- Reinforced Trade Connections with Asia-Pacific

While policies push to shorten the supply chain, surveys on the European and American companies nevertheless indicate a reinforced trade connections with the Asia-pacific region.

Firstly, both EU and US companies remain committed to the Chinese market. The 2021 Business Confidence Report by the EU Chamber of Commerce in China recorded its lowest figure of only 9% of the respondents (EU companies in China) stating their intention to redirect their investment elsewhere. Similarly, the US Chamber of Commerce in Shanghai indicated that 21% of respondents in 2020 considering diversifying their investment, down from 25% in 2019.

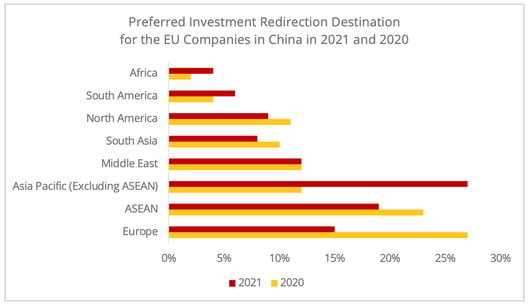

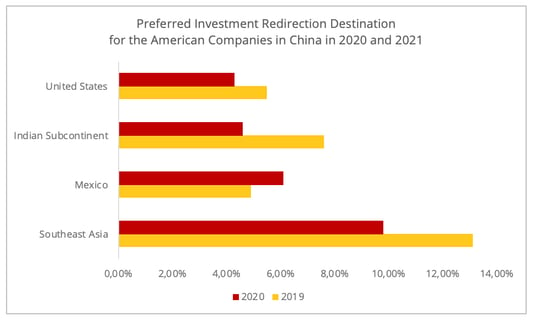

Secondly, the Asia-pacific region continues to be the top destination among the options for redirecting investment. Surprisingly, investment redirection to Europe dropped from the most preferred choice in 2020 to third place in 2021 (Figure 2). Reshoring to the US was only the fourth preferred option in 2020, following Southeast Asia, Mexico, and South Asia (Figure 3). This is due to a multitude of reasons, the relatively stable situation of the pandemic in Asia, the geographic proximity to China, and the newly concluded regional trade agreement, the RCEP.

Finally, strengthening ties with Asian partners forms part of both the EU’s and the US’s supply chain strategies. For instance, during their meeting in May 2021, the US and Korean leaders agreed to deepen their collaboration on semiconductors and EV batteries. The surge in the intention of European investment to non-ASEAN Asia pacific countries may also connote a stronger link with Japan or Korea. Moreover, the EU has recently resumed trade negotiations with India following the tension with China.

Figure 2 - Data source: 2021 & 2020 Chinese Business Confidence Report by EU Chamber of Commerce in China.

Figure 3 - Data source: 2020 and 2019 China Business Report, the American Chamber of Commerce in Shanghai.

- Green Supply Chain: Rail Freight and Multimodal Shipping

The ongoing changes have a decisive impact on the transport sector. "Resilient and sustainable transport plays a key role in facilitating international trade and safeguarding the EU's supply chains," said the European Commission in February in a communication on EU trade policy.

The strategic sectors identified in both reports favor a sustainable and digital transition of the transportation industry, which in return secures supply chain resilience. Rail freight and multimodal shipping, as “eco-friendly” shipping modes, are gaining growing policy support in the EU and the US.

The railway is now placed in the forefront of the EU’s Smart and Sustainable Mobility policy, as it aims to double the rail freight capacity by 2050. The emphasis is on the digitalization of the rail freight and infrastructure improvements. As priority goes to cross-border rail links, this also helps to remove the infrastructure bottlenecks in the Asia-Europe rail and multimodal freight connections.

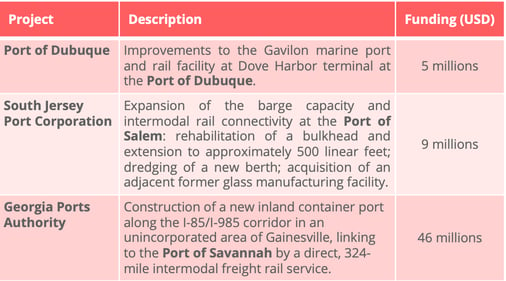

Similarly, rail freight and multimodal transportation are likely to be elevated through Biden’s new infrastructure plan (Table 4), even if it is not its main objective. The 80 billion USD investment in the rail passenger network will also benefit freight. Finally, the enhanced multimodal shipping connection to the East coast could increase the attractiveness of the Asia-US East Coast routes, whose share in connecting Asia has increased steadily over the years. Market interest in injecting more capacity in this route has also been noticeably observed this year.

Table 4 - List of Multimodal Projects funded by Biden Administration’s infrastructure plan - Data source: US Ministry of Transport.

(1) The percentage here refers to the share of the total value of imports of the most foreign dependent products.

(2) The EU also relies on the US supply of optical devices.

(3) The 25% tariff on various US products remains, but the EU has suspended a further increase of the tariff initially scheduled in June.