China-EU rail freight volumes on the main Eurasian corridor fell by 48% in the first semester of 2023, back to the pre-pandemic level of 2019.

It has been a rollercoaster ride for the China-EU rail freight market over the past three years. Following the exponential growth in 2020 and 2021 came the Russia-Ukraine war. Under the triple shocks of weak demand, the duration of the war, and the collapse of ocean freight rates, China-EU rail freight volumes in the main Eurasian corridor declined by 48% in the first semester of 2023, back to the pre-pandemic level of 2019 (Figure 1).

Figure 1- Data Source: EARI Index 1520

The geopolitical uncertainty curbed the China-EU rail freight market but drove up the China-Russian rail freight demand. According to the UTCL – the primary operator of the Eurasian corridor – the volume between China and Russia/Belarus surged by 180% in the first half of 2023. As a result, despite the plummeting China-EU rail freight activity, the China Railway Express (CRE) – the official name of the Chinese railway service between China and Europe – recorded 30% growth, reaching 936 thousand TEUs. China-Russia rail volume has now taken the lion’s share of the CRE.

Changes in the nature of the products transported

As for the China-EU rail freight market, there were both continuity and changes. On one hand, along with the continued erosion of demand, the volume has been further concentrated in one or two routes, Poland westbound and Germany eastbound. On the other hand, there have been changes in the nature of the products transported. Certain types of traffic whose shipments had surged in 2022 did not fare so well this year, such as chemical products (carbon blacks and test kits) westbound and milk powder eastbound. However, once again this year, some products deviated from this downward trend.

This is particularly true of the automotive sector eastbound, which contributed more than one-fifth of the total volume in the first half of 2023 in this direction. This can be attributed to the partial resumption of the shipment of vehicles by rail from Germany to China, which was halted entirely following the outbreak of war in Ukraine. However, this resumption has only enabled volumes to reach a third of their 2021 levels, against a backdrop of continuing geopolitical uncertainty and a contraction in the market for imported vehicles in China.

China's current consumption-driven economic recovery also created some new demand, albeit modestly, for shipping consumer products via rail to China. This aligns with the overall China-EU trade pattern following China’s reopening. Among the consumer goods transported by rail, the shipping of cosmetics products recovered and took the lion's share and saw a tripled growth in the first six months.

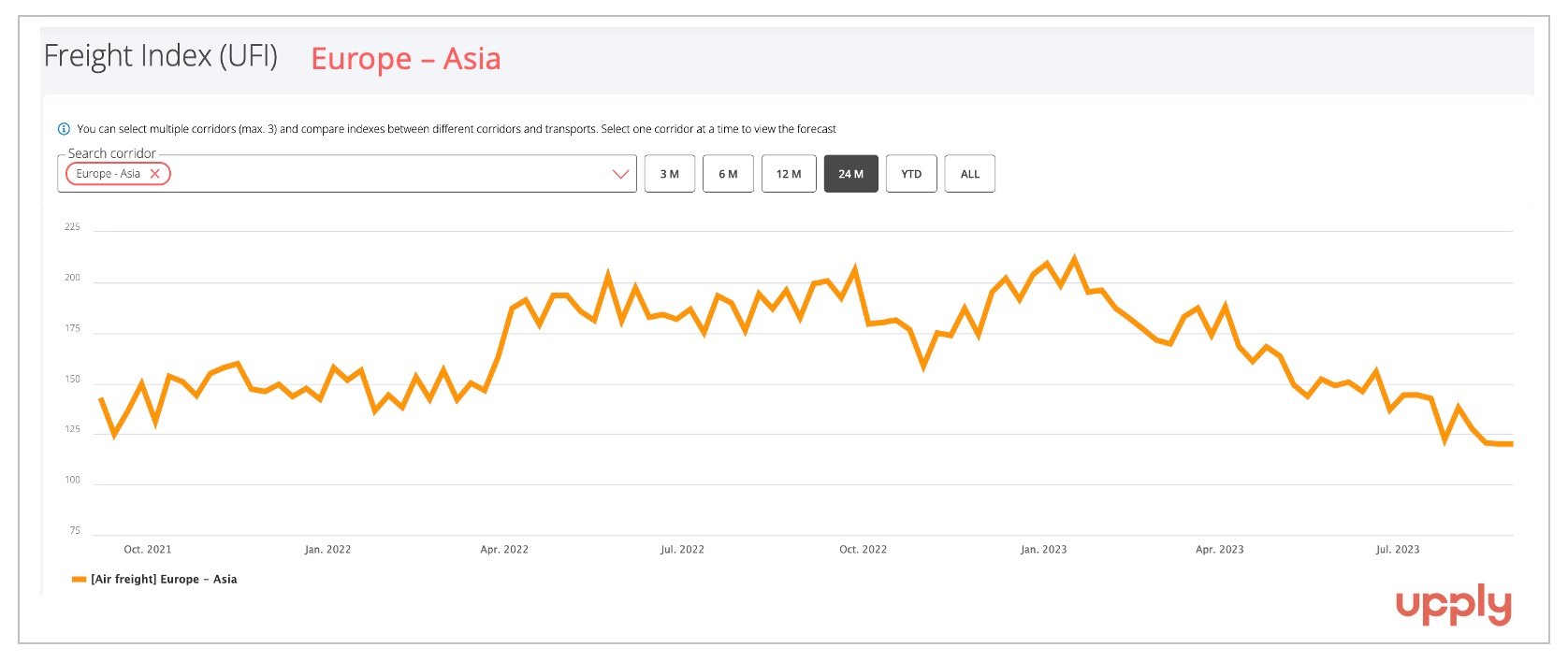

The shift from airfreight to rail freight has contributed to the increase. Indeed, airfreight rates from Europe to Asia have been falling in the past few months and are well below the 2022 level, according to Upply’s data (Figure 2). However, they are still higher than before the pandemic, which makes rail freight more attractive.

Figure 2 – Data source: Upply

In the westbound direction, China's policy of relaxing regulations to facilitate the shipment of new energy vehicles by rail since September 2022 has not yet translated into more dynamic growth in volumes, although China overtook Japan to become the world's largest exporter of cars in the second quarter of 2023. Nevertheless, the expansion of Chinese vehicle exports and the tight capacity of Ro/Ro vessels could create more demand for shipping electric vehicles via rail in the future. In the meantime, while vehicle shipping to the EU remains marginal, Chinese exports of diesel-powered vehicles via rail to Russia have boomed in the past few months.

A modest outlook

Among the aforementioned triple shocks, it is likely that geopolitical conditions and the sea freight market will not see any major developments from the current situation in the upcoming months. It is therefore the state of the world economy that should play the most important role among the three in the development of the rail freight market between China and the EU.

- The European Central Bank projects a 1.4% annual growth in imports for the Eurozone in 2023. The westbound shipping activities will therefore remain modest. Particularly as the plunging market for consumer electronic goods, which have long been the top products shipped via the China-EU rail freight connection, will most likely continue to affect the flow.

- Whether there is a more sustainable flow of consumer products in the eastbound direction depends on the extent of Chinese consumption recovery. However, the gloomy Chinese domestic market since the second quarter of 2023, together with a more conservative inventory strategy in the Chinese retail sector, overshadows this prospect.