BAROMETER. Global air cargo traffic increased by 8.3% year-on-year in November 2023. Freight rates have also risen on the main routes.

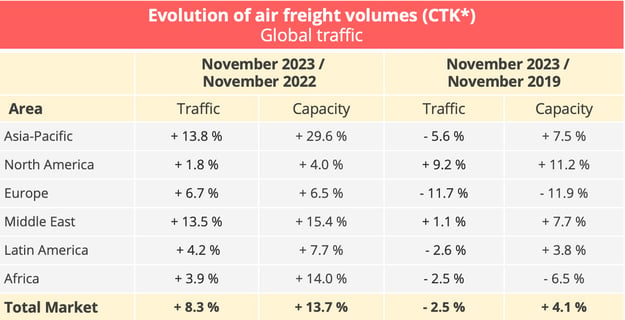

Global air cargo traffic reached 22.4 billion tonne-kilometres in November 2023, according to the latest data released by the International Air Transport Association (IATA). It thus increased by 8.3% year-on-year, which corresponds to the 4th consecutive month of growth and the strongest increase recorded since December 2021. In seasonally adjusted terms, the increase was 8.0%.

* FTK: freight tonne-kilometres - Data source: IATA - © Upply

The end-of-year trend is therefore quite satisfactory for the air cargo industry, although two caveats must be made. On the one hand, this performance can be explained in part by a base effect, as traffic was down sharply in 2022. On the other hand, traffic remains 2.5% below the pre-pandemic level of November 2019.

At the same time, freight capacity is continuing to grow very significantly. It reached 47.9 billion tonne-kilometres in November 2022, up 13.7% year-on-year, and 4.1% compared to November 2019. This rise is still mainly due to the increase in supply on board passenger aircraft. On international routes, this supply jumped by 28.8% to reach a capacity of 18.9 billion tonne-kilometres in November. During the same period, the supply on board all-cargo aircraft increased by only 1.2% to 18.2 billion.

Growth that benefits companies in Asia and the Middle East

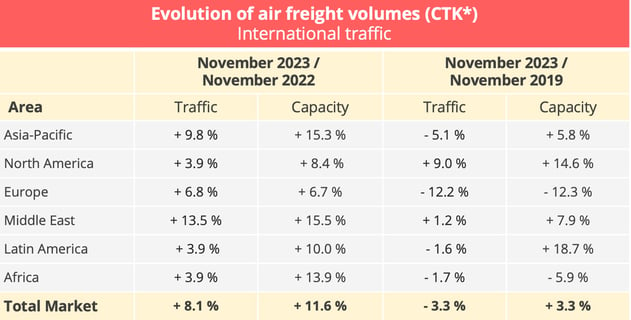

The increase in cargo traffic on international routes is only slightly lower than that of overall traffic. It stood at 8.1% in November 2023, with traffic still down 3.3% compared to the pre-pandemic level of November 2019. Supply is increasing, but also to a lesser extent.

* FTK: freight tonne-kilometres - Data source: IATA - © Upply

In November, the first prize for growth went to Middle Eastern airlines. The Middle East/Europe corridor, in particular, grew 23.5 percent year-on-year in November, making it the most dynamic corridor among the major air routes in global trade.

Asia-Pacific airlines are also benefiting from the rebound in activity. The Africa/Asia market grew by 13% (without significantly benefiting African airlines), the Middle East/Asia corridor by 12% and the Europe/Asia corridor by 8.7%. The intra-Asian market saw its first rise in 17 months, with year-on-year growth of 5.4% in November. Finally, the Asia/North America market posted an increase of 4.8%, still relatively modest compared to the average.

North American airlines are suffering from this situation, as well as from the relatively weak growth of the Asia/Europe market (+3%, which is nevertheless the first year-on-year increase in 13 months, according to IATA). This under-performance should be put into perspective, since American companies can also boast of 9% growth compared to the pre-pandemic level.

European airlines are doing quite well, benefiting from the performance of the Middle East/Europe corridors and, to a lesser extent, those between Asia and Europe, which offset the 1.8% contraction in the European domestic market. Another positive point for European airlines is that, although their traffic growth is lower compared to that of Middle East and Asia/Pacific airlines, it remains slightly higher than the growth of capacity, which preserves the load factor. Heavily affected by the consequences of the Russia-Ukraine war, European airlines consequently posted the largest drop in traffic compared to the pre-pandemic period, but again in line with the decline in capacity.

Adjustment of freight rates

According to IATA, yields, including surcharges, continued their upward trend (+8.9% compared to October). This is a logical development at this time of year, which is usually marked by a certain momentum in the run-up to the holidays, especially in the e-commerce sector between China and Western markets. Our Upply database, which lists prices charged on both the spot and contract markets, illustrates this dynamic between Asia and Europe. There was also growth on the Europe/Middle East and Europe/North America routes. Given the fact that capacity is growing faster than traffic, the increase is nevertheless contained. In addition, prices remain well below 2022 levels.

Source: Upply

IATA believes that the conflict in the Middle East and supply chain disruptions affecting container shipping could put further pressure on freight rates, which will be reflected in the data from December onwards. However, the first available data for this period do not seem to confirm this hypothesis.

Mixed Economic Fundamentals

The economic context is still rather unpromising. IATA recalls that the Purchasing Managers' Indices (PMIs) of manufacturing output and new export orders – two leading indicators of global air cargo demand – continued to hover just below the 50 mark in November, "with slight positive movements indicating a deceleration in the economic slowdown".

Inflation in major advanced economies continued to slow in November. On the other hand, a small rebound was noted in December, a sign that the situation remains fragile. China, on the other hand, posted negative annual growth in the consumer price index (CPI) in November, which is no more good news than hyperinflation is. Indeed, this is indicative of economic difficulties in China, where the recovery was weaker than expected after the end of the Zero Covid policy.

The air cargo industry therefore benefited from a slight peak-season effect at the end of the year, but 2024 is expected to get off to a rather sluggish start, due to the expected slowdown in global economic growth.