Global air freight traffic fell again in November 2022 both year on year and in relation to its 2019 pre-pandemic level.

The phenomenon is sufficiently rare as to warrant being underlined. In 2022, the air freight industry did not experience its traditional end-of-year peak season. It will be a number of weeks yet before we have the December figures but, in November, IATA noted an unusual phenomenon. Global demand fell in relation to the previous month, with a traffic total of 20.6 billion tonne-kilometres in November, compared to 21 billion in October. The slight increase on the September traffic total seen in October was not maintained, therefore, in November.

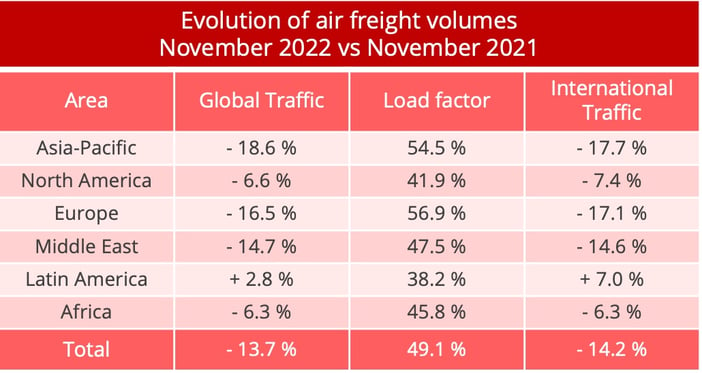

The November figures were 13.7% down year on year and 10.1% down on their November 2019 pre-pandemic level. The fall was even sharper in the international sector alone, where traffic was 14.2% down year on year, making it the biggest drop in monthly traffic year on year this year, according to IATA. On the basis of seasonally adjusted results, all the major trade corridors were affected by the reduction: Europe-Asia (-19.8%), Asia-North America (-18.7%), Middle East-Europe (-16.3%), Intra-Asia (-20.4%). North America-Europe routes held up a little better (-3.5%).

At the end of November, the traffic total for the year stood at 229.4 billion tonne-kilometres, which represents a 7.4% reduction on 2021 at the same point and a 1.5% reduction on 2019.

* CTK : cargo tonnes-kilomètres – Data source : IATA.

Situation under control

For the time being, the situation is being kept relatively well under control by the airlines, which are using their transport capacity cautiously. Global capacity was down 1.9% in November and stable in the international sector alone. It is well down, however, on its November 2019 level (-8.8% overall and -7.9% in the international sector alone).

The way that the airlines are managing their capacity is enabling freight rates to hold up well. Operators should, therefore, register satisfactory financial results in their cargo businesses in 2022 after a very good 2021.

Source : Upply

Worrying signs

Deteriorating economic conditions are nevertheless going to continue having an impact on the sector's performance. In the first place, even if inflation has begun to ease in the leading Western economies, thanks particularly to the fall in oil prices, it remains at high levels and is is continuing to affect household purchasing power and company production levels. Global demand risks being affected, therefore.

As regards air freight more specifically, new export orders in the leading economies are still below the 50 (no change) point in the purchasing managers' index, which means that cargo volumes are likely to show little growth. IATA said that Germany was nevertheless experiencing a "first improvement in its export orders since February 2022, signalling a degree of normalization after the months-long impact of the war in Ukraine," The United States and Korea also registered slight improvements in export orders.

The air freight business also faces another challenge. It needs to attract traffic from the container shipping industry, which now has capacity available at attractive rates. The gap in competitiveness between the two transport modes, which closed somewhat during the pandemic, is now growing again. That said, the shipping industry is still falling well short of the level of reliability expected by the market. From this point of view and also in terms of transit times, the air freight industry has an advantage. With stock levels high, however, it is difficult for it to exploit this advantage. It is, therefore, going to have to grin and bear things for some months to come.