The collapse of freight rates in the container shipping sector was confirmed in 2023. For the top ten container shipping companies, the impact has been greater than expected and has been felt more rapidly.

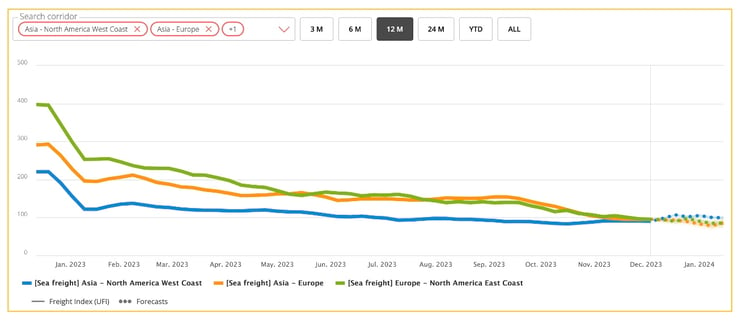

In 2023, the container shipping market was marked by the return of freight rates to pre-pandemic levels on most routes. The slump in rates at the start of the year has given way to a more gradual but ongoing decline.

Source: Upply

Supply and demand balance reversed

The slowdown in demand, aggravated by a still high but gradually declining inflation rate in Western countries, contributed to a reversal of the balance between supply and demand. Shipping companies with a strong presence on east-west routes suffered most proportionately from the turnaround in the market.

Although the collapse in demand played a determining role in the fall of container freight rates, the situation was aggravated by overcapacity, as the shipping companies gradually took delivery of the ships they had ordered during the period of prosperity from which they benefited in 2021-2022. This overcapacity will continue in 2024 and 2025, plunging the container shipping sector into an umpteenth structural capacity crisis.

All the models show that ships are being sent for demolition at a slower rate than new vessels are coming into service, killing off any hope of a long-lasting recovery in freight rates in the short term - short of a major external event like the arrival of Covid in 2020. If there was a major war, for example, causing ships to avoid the Suez Canal, there could be very serious implications for freight rates. The same would apply in the event that there was an open crisis over Taiwan.

What is certain is that another year of freight rates at 2023 levels would definitively wipe out the positive effect of the Covid years on the financial situations of container shipping operators, whether they be shipping companies or non-vessel operating common carriers (NVOCCs).

Business models redesigned

The current year began with an item of news which attracted a great deal of attention. Maersk and MSC announced that they were ending their alliance. Without waiting for the official date, MSC began acting independently of its Danish partner to a large extent in 2023. The Swiss-Italian company implemented a highly aggressive rates policy with the aim of acquiring additional market share, taking advantage of a lack of reaction from its direct competitors. It has been leading the race in terms of capacity in service since 2022 and, in 2023, it increased its lead.

In the meantime, Maersk and CMA CGM have relied more on a vertical integration business model, which should enable them to generate cargo volume and protect themselves from turbulence on the container shipping market by diversifying their activities. This model has not yet proved itself in current depressed economic conditions, however. As for the big "classical" international forwarders, they have emerged from the pandemic stronger than they were and are taking advantage of the decline in the market.

The next thing to watch out for will be the end of the block exemption from EU competition regulations which shipping consortia have been enjoying since 2009. The exemption will end in April 2024, but this should not cause a great deal of upset among the big shipping companies, since it does not mean that cooperation will no longer be allowed within the shipping alliances. Publicly at least, CMA CGM has assured that it will continue its joint operations with China's COSCO group for years to come.

The sovereignty argument

The current year was also marked by the announcement that South Korea's HMM group is to be sold. Its German rival, Hapag Lloyd, was interested but its offer was set aside in favour of bids from South Korean candidates. According to the South Korean press, two of the three companies selected, Harim Co. and Dongwon Industries, each offered to buy a 58% stake in its capital at the end of November. The third company, LX International, is understood to have finally decided not to make an offer because of the state of the shipping market and the general economic environment.

The rejection of Hapag Lloyd's offer is an indication of the increased importance states are attaching to shipping companies, which are seen as instruments of national sovereignty. This is true in Korea, but also in China, where COSCO serves the interests of the Chinese state.

Europe is no different. Over the last two years, CMA CGM has shown that it is ready to take on responsibility in this respect, by coming to the aid of French companies in difficulty, like GEFCO, Brittany Ferries and Air France. MSC is also playing the patriotic card. This autumn, it has signed two agreements in the rail sector, one with private sector operator Italo and the other with traditional public sector operator Ferrovie dello Stato (Trenitalia). It also invested in Italian air freight operator AlisCargo Airlines. More discreetly, the Maersk group continues to play a major locomotive role in the Danish economy.

The United States is an exception in this respect. Apart from Matson, which is not a pure container carrier, it has no major shipping company. Can its re-industrialisation policy survive much longer without it having a powerful operator in the container sector? That would appear to be difficult.

New geopolitical situation

The globalisation model, as it has existed for the last 30 years, is evolving at high speed as it runs into major crises. The days of seeing the macro-economic situation of the world solely through the lens of Western consumption of products manufactured in Asia are over.

Companies are now careful to diversify their supply sources to reduce risk. This strategy is starting to have a real influence on global trade patterns. The shipping companies are going to need to take this into account in their service offerings.

The world is more multi-polar than before but also more unstable. There is growing tension in many parts of the world. With the Russian-Ukrainian war, which began in February 2022, still in progress, the Israeli-Palestinian conflict has now made its appearance. These events could disturb world trade and the transportation of goods more generally. The situation is particularly tense in the Red Sea, the Gulf of Aden and the Strait of Hormuz following the start of the Israeli-Palestinian conflict but there are other geopolitical hot spots in a number of other regions of the world.

This deterioration in the international situation makes shipping companies and supply chain infrastructure generally more vulnerable to cyber attacks. This was not a new phenomenon in 2023 but events confirmed that the transport and logistics industries are choice targets for such attacks. The risk of cyber attacks against operators in these sectors has never been so great as it is today. The need to take account of this in companies' forward development plans will be one of the major IT challenges of the years to come.

The climate question

The climate emergency is increasingly featuring in the public debate, as emissions of gas from the combustion of fossil fuels continue to increase. Between the forced "degrowth" advocated by some and the green growth proposed by others, the debate remains open but it is incontestable that the climate question has become a central issue.

As a major emitter of CO², the freight transport sector has understood that it must involve itself resolutely in the energy transition. The movement seems to be under way, even if its objectives are still difficult to reach in the absence of a systemic approach. The shipping companies have taken advantage of the profits they made in 2021 and 2022 to invest in the "greening" of their fleets but there are still many uncertainties regarding alternative propulsion systems. Ammonia looks to have established itself as an alternative fuel, so long as the industry remains depend on combustion engines.

The European Union is procrastinating but is nevertheless taking a voluntarist approach to the struggle against climate change. A new deadline is coming up for the shipping sector. From 1 January 2024, the EU's emissions trading system will be brought into service in the shipping industry.

On 16 November, the European Parliament's transport and tourism committee also voted in favour of updating EU rules regarding the prevention of pollution by ships in European waters and imposing fines on the owners of offending vessels. "It would ensure all international standards on preventing illegal discharges from ships, developed by International Maritime Organisation, become part of EU law and as a result become more easily enforceable," the parliament said in a press release, adding, "MEPs supported the proposal to extend current EU rules prohibiting the discharge of oil and noxious liquid substances to include the discharge of sewage, garbage, and residues from scrubbers."

The revision of the directive on pollution from ships is part of a package of maritime safety measures presented by the European Commission in June 2023 with the aim of modernising and strengthening EU rules regarding maritime safety and the prevention of pollution.

To download the article in PDF format, please leave your contact details: