The first half of 2023 was marked by the return of overcapacity in the container shipping sector and, with it, slow steaming. This was not enough, however, to prevent freight rates from collapsing.

For the shipping companies, the violence of the collapse in freight rates was commensurate with that experienced by shippers when freight rates exploded in 2021. The shipping companies have been knocked for six during the first half of 2023. The turnabout in the market was expected but its intensity and the speed with which it occurred were much greater than they had expected.

Adaptability and reactivity will need to be the watchwords if the shipping companies want to minimise the damage and diversify, if they are able, into more profitable, related activities.

We sometimes hear people talking about a "return to normal" to describe the return of ocean freight rates to pre-pandemic levels, particularly on East-West trade routes. Two things need to be noted, however:

- 2019, which is often taken as a reference year, was a bad year for shipping company results on East-West routes.

- Since then, shipping companies' operating costs have increased by about 30%.

A real "return to normal" on regular shipping lines would require three conditions:

None of these three conditions currently applies on the East-West corridors. In this respect, therefore, it is, incorrect to talk about a return to normal, unless it is supposed that market operators have come to a consensus on some sort of new normal. Such a new normal would means shippers accepting "semi-regular" line services, with, for example, 60-day Europe-Asia transit times via The Cape and knockdown freight rates which barely covered shipping companies' operating costs. At a time when shipping companies' financial situations are deteriorating, such a new normal hardly appears viable.

Although it seems more suitable to talk about a return to abnormal rather than normal, it cannot be disputed that the same causes have the same consequences, and that this first half of 2023 is a new illustration of that.

1/ Long-term overcapacity

As an industry involving heavy capital investment, shipping can only think order newbuildings when the market is favourable for the shipping companies, which has only rarely been the case in recent decades. The exceptional revenues they collected in 2021 and 2022 incited the shipping companies to place massive orders for newbuildings. As Jan Tiedemann pointed out in a brilliant study published by Alphaliner in February 2023, shipyard orderbooks are currently at record levels.

The capacity deployed by the shipping companies is going to increase considerably in 2023 and 2024, since the arrival of new ships will only be partially covered by ships being taken out of service. But the new ships will be coming into service on a market which has gone into reverse. A first economic factor to be taken into account is that, after having overheated, consumption has fallen and east-west cargo volumes with it. Another structural phenomenon also needs to be taken into consideration. Even if Western economies clearly remain heavily dependent on China, the diversification of supply sources has become a strategic objective for shippers, who are determined to learn lessons from the pandemic. This trend has now become tangible. As a result, it will take the market 10 years or more to digest the new capacity.

That does not mean that the situation is fixed. Container shipping market leader MSC's is engaged in a frantic race for capacity as part of an offensive strategy which has increased the capacity of its fleet to close to 5 million TEU. Market share is gained on a declining market rather than on an expanding one. MSC has clearly set the temperature of the market and the other companies are following it as best they can by trying, in the absence of any real possibility of reducing rates, to differentiate themselves from their competitors by better quality of service and transit times or access to inland container parks.

2/ Shippers favour spot market

The introduction of the IMO's new carbon intensity rating rules has coincided with a need on the part of the shipping companies to manage their overcapacity. This means that there is a convergence between the environmental objectives and financial imperatives of the shipping companies, which have opted to slow down their ships very significantly. Shippers can hardly protest over this measure, which has been presented as an environmental one.

Lower ship speeds have not been enough, however, to stop the fall in freight rates in the first half of 2023, when demand was at a low ebb. This amounts to a failure on the part of the shipping companies, who had been hoping that the use of market discipline to control capacity growth would enable them to limit the reduction.

Given that fuel prices fell considerably during the pandemic, it cannot be excluded that some companies could try to gain a competitive advantage by setting up faster services again. This could prove to be pertinent for newly "nearshored" cargo, for which clients could be ready to pay higher rates to get shorter transit times.

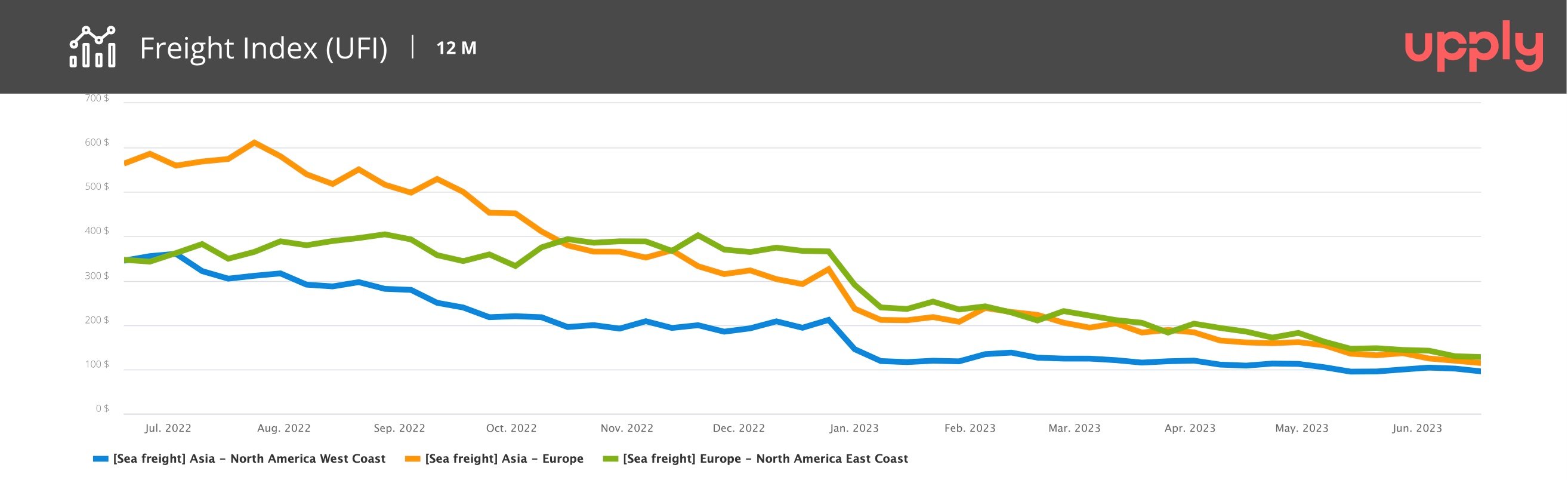

Spot and contract rates on Asia-Europe, Europe-North America East Coast and Asia-North American West Coast routes in the first half of 2023 - Base 100: January 2017. Source: Upply.

A final, notably feature of the first half was the unwillingness of shippers to give the shipping companies long-term cargo commitments. The two and even three-year contracts they signed at the height of the pandemic are now a thing of the past. When they have decided to sign a contract this year, shippers have opted to return to annual contracts.

The attractive rates available on the monthly spot market and their downward trend have persuaded most shippers to adopt a strategy of permanent renegotiation of rates. In this, they have the backing of forwarders, who, with rates falling, have recovered their added value as negotiators for their clients. On East-West routes, spots rates were on average 40% lower than new contract rates in the first half. In this situation, it is easy to understand why shippers are in no hurry to negotiate new annual contracts.

For the shipping companies, which are forced to sell space aboard their ships cheaply if they want to have a hope of loading what little cargo is available, this is clearly not beneficial from a financial point of view. Spot rates accounted for more than 40% of cargo transported on East-West routes in the first half, a level which is unprecedented.

3/ Climate favourable for digitalisation

Amid all this bad news for the shipping companies, there is one positive point. Increased interest in the spot market has led to much greater use of their digital systems. Shippers looking for a good deal are increasingly making use of the shipping companies' digital reservation systems.

For the time being, the shipping companies are not enjoying the financial benefit of this, but forwarders and shippers are adopting new digital habits, attracted by the ease of access they offer to the best rates. It would seem that a new digital freight transport cash purchasing system is emerging.

In the long term, this change of habit is an advantage for the companies. It enables them to build up customer loyalty and gather precious information enabling them to capture and manage physical cargo flows. The deeper knowledge of their clients it affords also offers them an opportunity to offer relevant additional, profitable services in such areas as customs control, logistics, pre and post-shipment transport and insurance.

It is also a way of safeguarding and speeding up customer payment procedures at a time when they are having to cope with a real financial shock.