The war in Ukraine is exacerbating the rise in energy prices and disruptions to supply chains that have emerged during the pandemic. These two factors will weigh on the evolution of transport prices and logistics costs in general.

Two years after the outbreak of the pandemic, which generated an awareness in Europe of issues concerning strategic independence, Russia's invasion of Ukraine painfully confirms the diagnosis. In the immediate future, these two major crises will lead to an unprecedented increase in logistics costs, and in particular transport prices. In the longer term, the economic and geopolitical recomposition accelerated by these events will necessarily mean the restructuring of supply chains.

CONTENTS

- General increase in transport prices

- Inflation of production costs

- A violent shock for carriers

- The vulnerability of the supply chains in question

- Threats and opportunities for energy transition

- The risk of a decline in demand

1/ General increase in transport prices

Shippers are experiencing an unprecedented crisis. Over the past two decades, logistics schemes have been built on the premise of relatively inexpensive transport (obviously with disparities depending on the nature of the products). The energy transition gave a glimpse of some financial efforts to come. But as public policies remain relatively lenient at this stage, the impact on transport prices will be unlikely to transform the architecture of supply chains.

The correction will finally have come from exogenous factors, and with a brutality that no one would have imagined even three years ago. The 2022 transport budget is completely different to that of 2019. The Covid-19 pandemic has led to a surge in freight transport prices. The war in Ukraine is therefore not the triggering factor but rather an aggravating factor, which extends the phenomenon and prolongs it over time.

Transport price inflation first affected container shipping and air freight. It is now gaining momentum in European road transport.

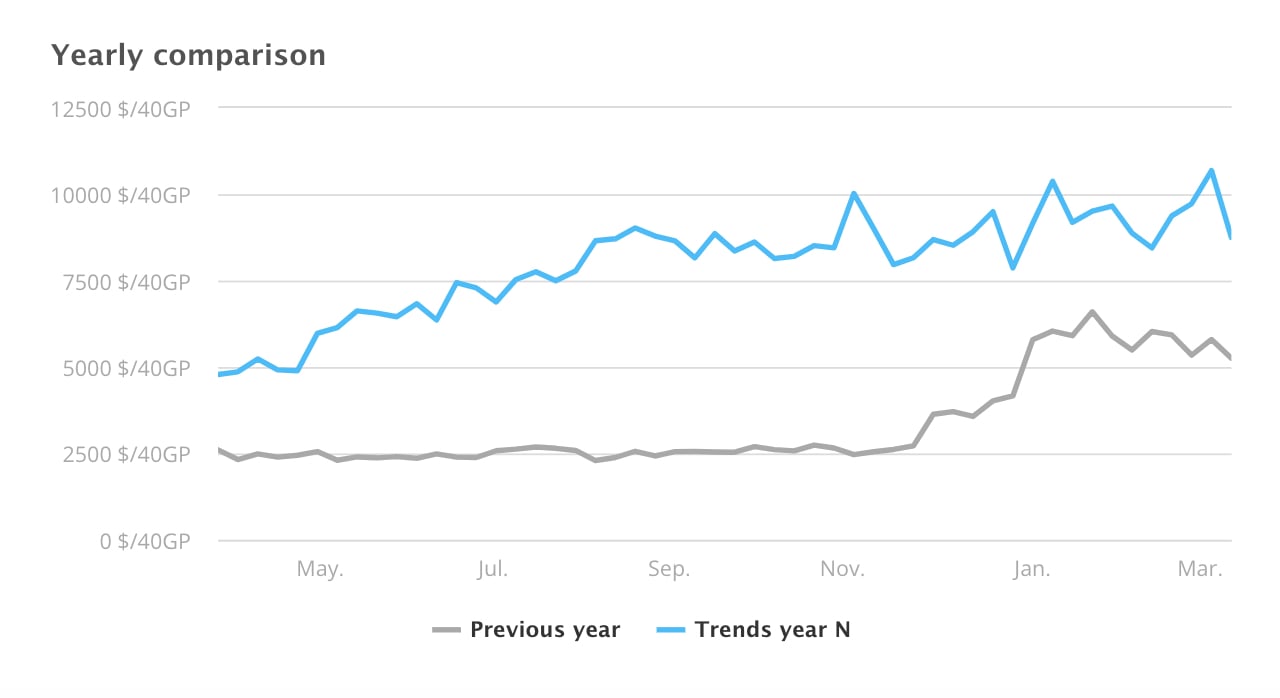

- In maritime container transport, companies entered this health crisis with depleted treasury levels. In 2020, they were able to judiciously manage their capacity to avoid collapse. A discipline that they maintained in 2021 even when demand recovered strongly, this has allowed them to increase prices on the main corridors worldwide, regain control of their customer portfolio and generate profits on an unprecedented scale. Between Asia and Europe, the average rate basket has quadrupled in three years to around 6,000 to 7,500 USD per 40' container, with peaks on FAK rates well above this figure.

Evolution of the freight rate for a 40' container in port to port, including surcharges, between Shanghai and Rotterdam – Source: Upply

While a slight lull was expected after the Chinese New Year, the geopolitical context related to the war in Ukraine is maintaining price levels, especially via surcharges. In a report published on 16 March, however, UNCTAD estimates that upward pressure should soon affect maritime transport prices.

- In air transport, the situation is a little different. In 2020, the paralysis in passenger air transport, which usually carries close to 60% of the world's cargo, led to a drastic drop in supply while demand remained dynamic, especially for the transport of personal protective equipment. Freight rates then rose very sharply. The trend continued in 2021 as the very dynamic recovery in consumption favoured the use of air freight to meet demand. While the average unit revenue increased from $1.79/kg to $2.71 between 2019 and 2020, it peaked at $3/kg in 2021 according to estimates by the International Air Transport Association. In its forecast published last October, IATA predicted a decline for 2022 to $2.67/kg. But the Ukrainian conflict changed the situation, weighing on costs and capacity. IATA has not yet published an updated forecast, but its director has already announced an increase in prices, in proportions "still impossible to measure". The sector also remains at the mercy of the restrictions to activity that regularly hit China as part of its "zero Covid" strategy.

- In road transport, the economic recovery also favoured the increase in European transport prices in 2021. However, the increase was more limited than in international transport. This situation should change. The sector is indeed caught up by the vital need to pass on cost increases.

- Finally, in rail freight transport, the conflict in Ukraine is disrupting the promising Silk Roads, in particular by calling into question investment projects in Ukraine.

2/ Inflation of production costs

In 2021, the increase in transport prices was mainly driven by the rapid rebound in demand, itself favoured by massive stimulus packages. This has created an imbalance in relation to the available supply and therefore a favourable balance of power for the carriers.

The rise in freight rates was also fuelled by the impact, albeit partial, of the inflationary pressures, in particular on energy and commodity prices as a result of the V-shaped economic recovery. Central banks hoped that this overheating would gradually be regulated when supply and demand were rebalanced through the improvement in congestion and shortages caused by the Covid-19 pandemic. But the outbreak of war in Ukraine is totally upsetting the outlook.

Oil prices, which had already started to rise in 2021, have risen sharply in recent weeks due to the conflict between Russia and Ukraine. The market is very volatile, but overall, prices appear to be settling at more than $100 per barrel. The situation is critical enough for the International Energy Agency to have published on 18 March an emergency plan calling for 10 measures to reduce global oil demand by 2.7 million barrels per day and thus reduce the risk of a critical shortage.

The situation is equally threatening for gas, as Europe is particularly dependent on Russian production.

- Increase in prices of industrial and agri-food commodities

Apart from energy prices, other factors contribute to the rise in production costs. “Although slowing down, prices in euros of industrial raw materials increased again sharply in February (+5.1% after +7.7% in January), in conjunction with the prices of mineral materials (+5.8% after +7.4%). Ferrous metal prices slowed down but remained dynamic (+7.5% after +12.8%), as did non-ferrous metal prices (+5.2% after +7.7%)", underlines the INSEE in a note published on 18 March.

Prices of agro-industrial and imported food commodities also showed a predominantly upward trend in February, although there has been a deceleration. On this last point, the conflict in Ukraine is expected to have a heavy impact. The Russian Federation and Ukraine are global players in agri-food markets. Together, these countries hold a 53% share of world trade in sunflower oil and seeds, 27% for wheat, 23% for barley, 16% for rapeseed and 14% for corn, the UNCTAD report said.

The inflation that economists had hoped would be provisional and measured seems to be long-term and growing. In its winter 2022 economic forecast, the European Commission has revised its outlook for price increases upwards. For the entire year, inflation is expected to be 3.5% for the Eurozone, compared to an anticipated increase of only 2.2% in its previous forecast published in autumn 2021. But these figures seem already quite modest. The annual inflation rate in the euro area stood at 5.9% in February 2022 and 5.1% in January, while a peak of 4.8% had been expected in the first quarter of 2022 in light of the record rate of 4.6% reached in the fourth quarter of 2021. In the United States, inflation was 7.9% in February and 7.5% in January.

This context favours the rise of wage claims. The transport and logistics sector is a labour-intensive sector, which was already experiencing recruitment difficulties before the crises. The upward pressure on wages will be all the greater, and will therefore weigh on the cost balance in 2022.

3/ A violent shock for carriers

The inflationary shock is obviously difficult for carriers to absorb, but there are however disparities. In container shipping, companies have improved their financial situation during the pandemic and thus have some flexibility, even if their operating costs are increasing. They continue to manage capacity deftly, and pass on fuel increases through fuel surcharges.

The situation is more reserved in the other sectors. In the air transport sector, while a few all-cargo airlines have been able to generate exceptional profits, the financial situation of conventional airlines, which provide most of the capacity, remains catastrophic after two years of the pandemic. Margins have recovered in freight activity, but this remains insufficient to ensure the profitability of the sector. On top of this, air transport remains highly vulnerable to crisis situations. The surge in fuel prices is very bad news for the sector, especially as the Russia-Ukraine conflict is forcing airlines to avoid flying over Russia and thus increase flight times between Asia and Europe.

Finally, in road transport, a sector with particularly low margins, the situation is very tense. Energy prices are soaring, whether it is petrol or gas for those who have taken this path to energy transition. In addition, the shortage of drivers is not diminishing, especially in Eastern European countries where the Ukrainian workforce was a significant pool of labour. Finally, the price of transport equipment is also subject to strong inflationary pressures: manufacturers are passing on, at least in part, the rising costs of raw materials and essential components such as semiconductors. Professional federations are sounding the alarm throughout Europe. If the energy trends observed over the last two months continue, the increase in the overall costs for French carriers in 2022 could reach 12%, recently declared Florence Berthelot, General Delegate of the employers' organisation FNTR, on the set of the news channel FranceInfo. Companies are threatening to put themselves out of business if they are unable to pass on a significant part of the additional costs. In France, the government has just granted emergency aid of €400 million to the sector.

4/ The vulnerability of the supply chains in question

The current situation is all the more delicate as shippers, like carriers, are hit hard by the increase in their production costs. The increase in energy prices is very bad news, especially in industry. That of raw materials too. Negotiations with carriers are therefore likely to be tense, with the capacity of absorption by the final consumer being kept in mind.

On the other hand, the new global crisis triggered by the war in Ukraine comes at a time when the sanitary situation is far from being stabilised. Supply chains have not yet regained the operational fluidity of the pre-pandemic period. While congestion is decreasing, it has not completely disappeared. Nor is the virus, and it is far too early to speak of a post-pandemic context. As part of its Zero Covid strategy, China continues to confine certain areas, partially or totally, at the risk of disrupting production. Foxconn, Apple's main supplier, announced in mid-March that it was pausing its activities in Shenzhen's Chinese technology hub due to sanitary restrictions.

For shippers, the situation is all the more difficult to manage as lockdowns, which lead to temporary production stoppages, are often put in place by local authorities with very little warning, which makes it impossible to activate alternative solutions. On the contrary, Ukraine and Russia are not major sources of production for manufactured goods. But the conflict is a new source of disruption for sea, air, rail, and road routes.

The outbreak of the Covid pandemic has generated a real reflection on the questions of sovereignty in Western countries, and also very concrete beginnings of a response to this. In both the United States and Europe, efforts are being made to identify the strategic areas in which it is necessary to reduce dependence by promoting a certain regionalization of supply chains. In the semiconductor sector, the American giant Intel has announced an investment plan of 80 billion euros in the European Union over the next ten years, and will install a factory in Germany.

5/ Threats and opportunities for energy transition

In the same way that the Covid-19 pandemic is having an accelerating effect on the reconstitution of industrial sectors in Europe or the United States in certain strategic areas, the war in Ukraine is brutally raising awareness that the energy transition is not so much a question of virtue as a guarantee of economic sustainability.

It also highlights the need to not approach the issue mainly through the prism of energy substitution, but also from the angle of sobriety. As such, Samada, Monoprix's logistics subsidiary, gave a particularly enlightening testimony during the Ceremony of the Kings of the Supply Chain organised on March 17 by Supply Chain Magazine. As part of a project to centralise logistics activities for non-food products, the brand worked with Prologis to put into operation the world's first certified carbon-neutral logistics platform. Particular attention has been paid to energy consumption, notably in terms of lighting and heating. On this last point, the use of geothermal energy has made it possible to "turn off the gas". A solution that Samada's managers have doubly welcomed today.

This example illustrates the potential gains and room for manoeuvre available to transport and logistics players. But it also shows that the transition can only be made at the cost of heavy investments that will require special support for smaller companies.

In the short term, UNCTAD fears there will be a step backwards. "The significant increase in oil and gas prices may shift investment back into extractive industries and fossil fuel-based energy generation, running the risk of reversing the trend towards renewables documented over the past 5–10 years," the report said.

6/ The risk of a decline in demand

The current inflationary spiral could, if confirmed, break the growth dynamic. In its forecast for winter 2022, the European Commission has already revised the pace of increase in the Eurozone's GDP downwards, from 4.3% to 4%, in its forecast published in the autumn. If increases in production costs are reflected in selling prices, choices will have to be made, especially for the poorest households, at the risk of generating a negative shock in demand. Companies are also concerned by these questions. The fertilizer manufacturer Yara announced at the beginning of March the suspension of production in its factory in Le Havre and in Ferrara in Italy, due to the rise in gas prices, an essential component of nitrogen products.

The effect of the war in Ukraine on agri-food commodities is also "particularly worrying", says UNCTAD. Some countries are highly dependent on agri-food products from the Russian Federation and Ukraine. "For example, the share of imports from the Russian Federation and Ukraine – as a percentage of total imports of wheat, corn, barley, colza, sunflower oil and seeds – is 25.9% for Turkey, 23% for China and 13% for India," declared UNCTAD.

Beyond the human drama it represents, the conflict in Ukraine is a new major shock for a still convalescent world economy. Supply chains will pay the price and have to reorganise. It is a question of getting into working order to respond to the new geopolitical situation of flows, but also to the emergence of a world where the notions of energy sobriety and strategic independence have become central to sovereignty.